BCG — Boston Consulting Group

By Giambattista (“GB”) Taglioni, Pia Tischhauser, Tjun Tang, Christopher Freese, and Jean-Christophe Gard

JULY 28, 2020

In the midst of this unprecedented crisis, insurers have the opportunity to transform and create sustained value, but they must move quickly, be bold, and focus on long-term results.

In the past four downturns, 14% of companies, on average, were able to increase both their sales growth and EBIT margin despite the challenging circumstances.

To build advantage in adversity, insurers must embrace what we call bionic distribution,

- blending human talent

- with digital technologies

- in new ways to create fast, intuitive, and digitally enabled experiences for customers.

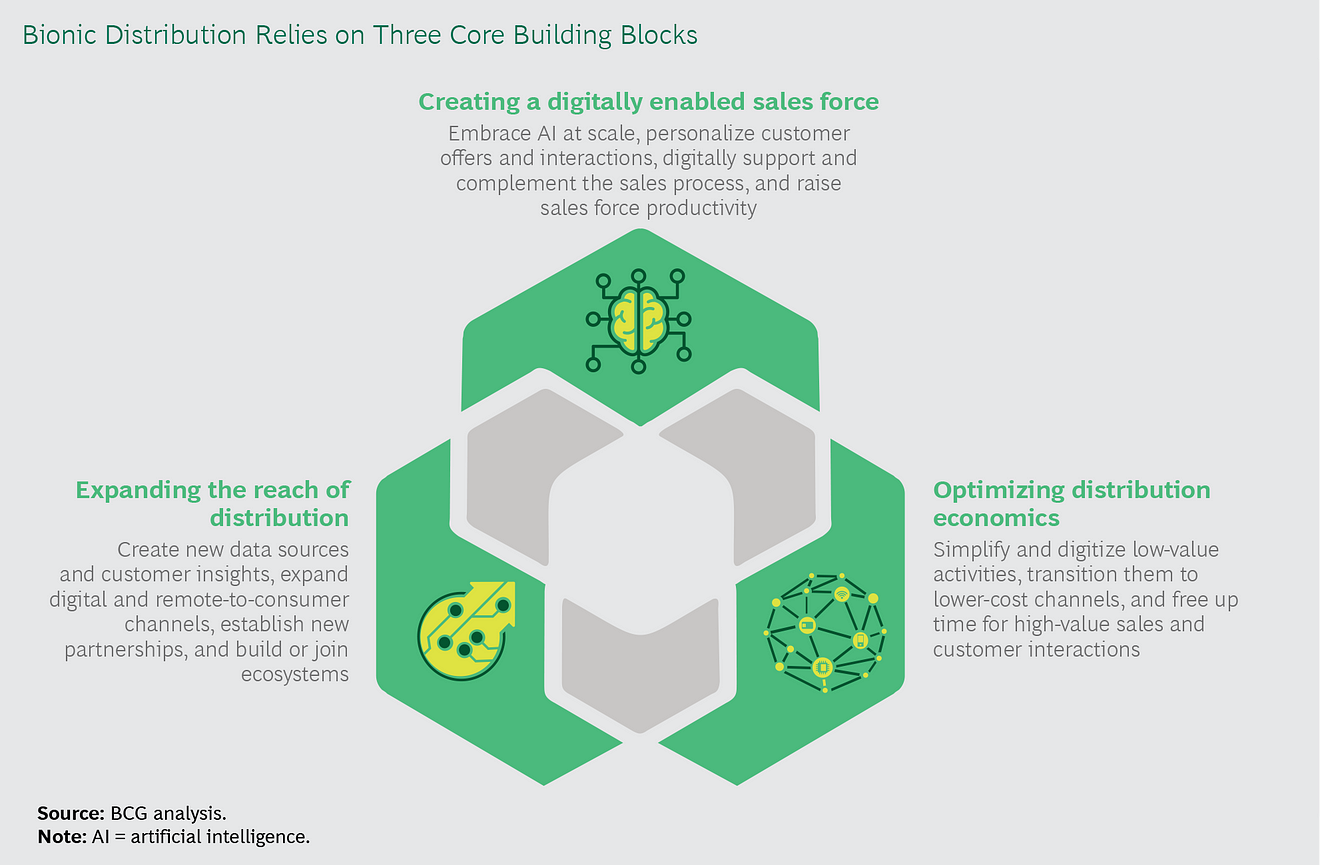

Bionic distribution relies on three core building blocks:

- creating a digitally enabled sales force,

- expanding the reach of distribution, and

- optimizing distribution economics.

CUSTOMER EXPECTATIONS ARE CHANGING QUICKLY

After months of extraordinary lockdowns, economies have entered a very delicate phase that we call the fight phase. Businesses must determine how to bring employees back to work sites and how to interface with customers while keeping the infection rate under control.

BCG expects the fight phase to last 12 to 36 months. The COVID-19 pandemic has already changed what customers want from companies, including insurers. How customers want to engage with insurers and where they choose to spend their money has also shifted. We believe these changes will persist.

- What Customers Want. Customers are looking for simple, transparent products that are presented in an intuitive and straightforward way. They also want options — such as payment flexibility should they become unemployed and the ability to switch features on and off depending on usage — that reflect their current reality.

- How Customers Want to Engage. With prolonged social distancing, digital platforms will become the new shopping malls for many product categories. Although traditional insurance agents and brokers will surely survive, they must learn how to work in an omnichannel model. Carriers must enable customers to move easily between digital and face-to-face engagements without interruption or inconvenience.

- Where Customers Choose to Spend Their Money. As often occurs during a crisis, we are seeing a flight to quality. In the wake of the pandemic, customers have turned to established and trusted insurance brands or to innovative digital powerhouses (such as Tencent and Alibaba in China) with robust digital ecosystems that include insurance. Many InsurTech startups have struggled to keep momentum because lower revenues have hurt liquidity and hindered their ability to invest, in some cases raising concerns about their long-term viability.

THE THREE BUILDING BLOCKS OF BIONIC DISTRIBUTION

For early adopters, bionic distribution has been a game-changer.

- They have boosted productivity by 15% to 20%,

- cut the time to market by half or more,

- improved the net promoter score by 20 to 40 percentage points, and

- lifted revenue by 5% to 10%.

To achieve these benefits, insurers must build their capabilities. (See the exhibit.)

- Create a digitally enabled sales force

- Expand the reach of distribution

- Optimize distribution economics

1.Create a digitally enabled sales force.

To reignite sales and expand margins, carriers must fundamentally change the way they think about distribution.

Traditional omnichannel and multichannel methods do not have the agent as the “superhero” or navigator at their core. A bionic distribution model, however, deploys agents who can add value at key moments in the customer journey and who are supported by an easy-to-use digital experience when their expertise and assistance is not needed. This means simple products and low-value activities should be fully automated and migrated to digital channels, while complex, high- margin, bespoke activities are managed by people who are supported by digital platforms and tools. (See the sidebar “Three Forms of Bionic Distribution.”).

Insurance companies have been investing in advanced analytics for years-and now is the time to monetize these capabilities by driving frontline adoption. With a digitally enabled sales force, insurers can leverage advanced analytics and AI to reimagine customer journeys, personalize the customer experience, and build modular insurance products.

- Reimagine customer journeys. By using data-driven insights, insurers can streamline the customer journey and substantially improve conversion rates. A leading insurer is using advanced analytics to mine the data it receives from a banking partner and significantly reduce the number of questions prospective customers must answer in order to receive a quote. By using AI, the company was able to automate a rote task, enhance its quote accuracy, and simplify the customer experience.

- Personalize the customer experience. Sophisticated algorithms are enabling insurers to deliver the right product at the right time with the right message and in the right channel. By creating touch points that anticipate, rather than react to, customers’ needs, companies can reduce churn, increase conversion rates, and catalyze cross-selling and upselling. A European multinational insurance firm is using AI to track customers’ concerns, questions, and sentiments across social media platforms, and it is shaping digital offers accordingly. Similarly, a bancassurance player is using AI to combine transaction data with life event triggers (such as the birth of a child or the purchase of a new house) to create more targeted product offerings. Using such techniques, companies have reduced churn by 17% and generated 15 times more revenue from cross-selling.

- Build modular insurance products. A digitally enabled sales force is better equipped to sell modular products- offerings that can be pieced together to suit each customer’s needs and quickly modified with on-off functionality as the customer’s needs change. AI also makes it possible for insurers to adjust coverage on the basis of a customer’s real-world behavior and its associated risks.

2.Expand the reach of distribution.

The insurance industry has historically been structured around product verticals, but customers are demanding a simpler, integrated journey. In addition, an inherent weakness of the insurance industry is that interactions with customers occur less than a handful of times per year.

As insurers fight to stay relevant and visible to their customers, ecosystem partnerships offer an opportunity to expand their role beyond product placement. Partnerships can give insurers access to new proprietary data, which they can use to deepen their customer relationships and win new customers. As the amount of ecosystem data grows, thanks to more frequent interactions, insurers can offer customers a better experience with more personalized product offerings, rewards, and service, delivering it in the right channel (such as through the web, mobile device, or email) and at the right moment (on the basis of location and time of day, for example).

Using this approach, insurers can double or triple their penetration across all market segments and boost conversion rates by three to five times. Ecosystem partnership opportunities are particularly relevant in the automotive, connected homes, and digital marketplaces. Examples vary widely: A European reinsurance company partnered with a multinational furniture retailer to provide bespoke, white-label home insurance. And a multinational insurer customized its products to fit each of its distributors’ platform-specific customer journeys, creating an integrated ecosystem and a seamless experience for users.

In addition to creating new partnerships and ecosystems, insurance companies have an opportunity to expand the reach of their direct channels (both online and remote-to-consumer channels) when targeting digital natives or selling simple products. During the pandemic, new digital offerings have been quite successful in many regions, and we expect this trend to continue, or even to accelerate, in the postpandemic era.

3.Optimize distribution economics.

Insurers have a unique opportunity to reduce distribution costs. Insurers, in both life and nonlife markets, have been wrestling for years with the need to reduce costs. In the wake of the pandemic, and with today’s lower-for-longer rates, cost reduction has become an imperative. This is particularly true for companies operating in developed economies and low-growth markets. In emerging markets, where growth rates are still in the double digits, the pressure to improve cost productivity has been less intense.

Distribution accounts for approximately two-thirds of insurance costs, and it has been relatively hard to tackle as distribution partners-agents, advisors, and brokers-have vehemently resisted any cuts. With bionic distribution, insurers can reduce distribution costs by digitizing activities that add little value, transitioning to lower-cost channels, and supporting sales representatives with digital and AI tools to be more productive. Ultimately, the goal is to create a smaller, more productive sales force, supported by digital channels (such as online platforms and remote advice centers) to reach a larger number of customers.

Conclusion

The stakes are high in a crisis-and smart business decisions are more critical than ever. In previous downturns, 14% of companies, on average, were able to grow their top and bottom lines and emerge stronger.

By implementing AI at scale, becoming bionic, and building strong digital ecosystems, insurers can accelerate the digital imperatives that will create a lasting competitive advantage.

About the authors

Giambattista (“GB”) Taglioni; Managing Director & Senior Partner; New York

Pia Tischhauser; Managing Director & Senior Partner; Global Leader, Insurance Practice; Zurich

Tjun Tang; Managing Director & Senior Partner; Hong Kong

Christopher Freese; Managing Director & Senior Partner; Berlin

Jean-Christophe Gard; Managing Director & Senior Partner; Paris

APPENDIX —THREE FORMS OF BIONIC DISTRIBUTION

Bionic distribution models can be viewed on a spectrum, from a digitally enhanced face-to-face model to one that is fully digital:

- Digitally Enhanced Face-to-Face Model. In this model, agents and advisors operate at the center of a web of channels, offering the convenience of digital self-service platforms that are supplemented by digital tools and remote interactions. Insurers need to adapt their wholesaling model to this new breed of hybrid agents and ensure that they have the digital resources and skills necessary to combine real-world and digital interactions. The role of the agent is changing, moving from prospecting and selling individual policies to becoming the navigator, the planner, and the advisor who can help customers with a broader set of needs. With the right digital tools for information sharing and transactional support (including, e-application and e-signature apps), agents can double productivity.

- Remote-to-Consumer Model. In this model, agents and advisors work remotely, interacting with customers via video chats, phone calls, texts, or emails and supported by a digital platform that allows for co-browsing and content sharing. This model is best suited for mass-market retail and small and midsize enterprise accounts. In the US, where distribution is largely through third parties, distributors are building remote-to-consumer models. (Merrill Edge is an example of a remote-to-consumer model for retail investors.) In other regions, where distribution relies more on captive models, insurers are equipping their distribution with remote capabilities and new data-driven digital tools. Some insurers are experimenting with staffing these new remote-to-consumer models with salaried employees, with high variable pay, to further reduce distribution costs.

- Fully Digital, Direct-to-Consumer Model. This model is best suited for simple products, such as auto coverage; customers are familiar with the product, and they are shopping for a competitive price. Digital channels also often serve as the entry point for customers who want to research more complex products and then complete their purchase through another channel. Therefore, ensuring a seamless customer experience across channels can be a strong differentiator.

Originally published at https://www.bcg.com on July 24, 2020.

To download the PDF, open the URL below: