National Bureau Of Economic Research

Working Paper 30857

Nikhil Sahni, George Stein, Rodney Zemmel and David M. Cutler

January 2023

The paper represents the views of the authors and not any entity with which they may be affiliated. The views expressed herein are those of the authors and do not necessarily reflect the views of the National Bureau of Economic Research.

NBER working papers are circulated for discussion and comment purposes. They have not been peer-reviewed or been subject to the review by the NBER Board of Directors that accompanies official NBER publications.

EXECUTIVE SUMMARY [by Joaquim Cardoso MSc]

ABSTRACT

- The potential of artificial intelligence (AI) to simplify existing healthcare processes and create new, more efficient ones is a major topic of discussion in the industry. Yet healthcare lags other industries in AI adoption.

- In this paper, the authors estimate that wider adoption of AI could lead to savings of 5 to 10 percent in US healthcare spending — roughly $200 billion to $360 billion annually in 2019 dollars.

- These estimates are based on specific AI-enabled use cases that employ today’s technologies, are attainable within the next five years, and would not sacrifice quality or access.

- These opportunities could also lead to non-financial benefits such as improved healthcare quality, increased access, better patient experience, and greater clinician satisfaction.

- We further present case studies and discuss how to overcome the challenges to AI deployments.

- We conclude with a review of recent market trends that may shift the AI adoption trajectory toward a more rapid pace.

In this paper, the authors estimate that wider adoption of AI could lead to savings of 5 to 10 percent in US healthcare spending — roughly $200 billion to $360 billion annually in 2019 dollars.

OVERVIEW:

Can artificial intelligence (AI) improve productivity in healthcare? That is a central question in the United States and the focus of this paper.

In the United States, healthcare is considered too expensive for what it delivers. Businesses are looking to manage their costs, and healthcare spending is a large and growing expense.

As healthcare spending grows in the public sector, it crowds out other governmental budget priorities.

Previous research has found that healthcare in the United States could be more productive — both costing less and delivering better care (Berwick et al., 2012[1]; Sahni et al., 2019[2]). AI is likely to be part of the solution.

The improvement in US healthcare productivity could manifest in several ways.

1.Reducing administrative costs is one example.

Administrative costs are estimated to account for nearly 25 percent of all US healthcare spending (Sahni et al., 2021)[3]; AI could reduce this burden.

2.Harnessing clinical knowledge to improve patient health is a second way.

Medical knowledge is growing so rapidly that only 6 percent of what the average new physician is taught at medical school today will be relevant in ten years (Rajkomar et al., 2019)[4].

Technology such as AI could provide valuable clinical data to the clinician at the time of diagnosis.

3.Improving clinical operations is still another example.

Operating rooms (ORs) are one of hospitals’ most critical assets.

Yet inefficient operations can result in wasted hours, leading to excessive building of space, hindering patient access, degrading the patient experience, and reducing hospitals’ financial margins.

In this paper the authors focus on two questions about AI.

1.First, how much might be saved by wider adoption of AI in healthcare?

To answer this, we estimate potential savings by considering how AI might affect processes for three stakeholder groups — hospitals, physician groups, and private payers.

For each stakeholder group, we illustrate AI-enabled use cases across both medical and administrative costs and review case studies.

Using national healthcare spending data, we then scale the estimates to the entire US healthcare industry.

We find that AI adoption within the next five years using today’s technologies could result in savings of 5 to 10 percent of healthcare spending, or $200 billion to $360 billion annually in 2019 dollars, without sacrificing quality and access.[5]

We find that AI adoption within the next five years using today’s technologies could result in savings of 5 to 10 percent of healthcare spending, or $200 billion to $360 billion annually in 2019 dollars, without sacrificing quality and access.[5]

For hospitals, the savings come largely from use cases that improve clinical operations (for example, operating room optimization) and quality and safety (for example, condition deterioration management or adverse event detection).

For physician groups, the savings also mostly come from use cases that improve clinical operations (for example, capacity management) and continuity of care (for example, referral management).

For private payers, the savings come largely from use cases that improve claims management (for example, auto-adjudication or prior authorization), healthcare management (for example, tailored care management or avoidable readmissions), and provider relationship management (for example, network design or provider directory management).

While we only quantify cost savings in this paper, there are additional non-financial benefits from the adoption of AI, …

… including improved healthcare quality, increased access, better patient experience, and greater clinician satisfaction.

2.The magnitude of these savings raises a second question: if AI in healthcare can be so valuable, why is it not in greater use?

At the organizational level, in our experience, there are six factors for successful AI adoption.

AI’s limited uptake can be partly explained by the difficulty of addressing these factors, such as the failure to create “digital trust” with patients.

In addition, we discuss industry-level challenges such as data heterogeneity, lack of patient confidence, and misaligned incentives.

Recent market trends, such as increasing venture capital and private equity investments, may increase the rate of AI adoption in the near future.

The paper is organized as follows.

- Section I outlines the scope of potential uses of AI in healthcare.

- Section II lays out how AI might be used for the three specific stakeholder groups — hospitals, physician groups, and private payers — and presents case studies as examples.

- Section III estimates the annual net savings that might result from adopting AI across all of US healthcare.

- Section IV considers the challenges to greater adoption of AI, and

- Section V discusses how market trends may change the decisions that organizations make about adopting AI.

- The final section offers concluding thoughts.

Conclusions:

The promise of AI in healthcare has been a topic of discussion in the industry for more than a decade. But its potential has not been quantified systematically, and adoption has been lacking.

The authors estimate that AI in healthcare offers a $200 billion to $360 billion annual run-rate net savings opportunity that can be achieved within the next five years using today’s technologies without sacrificing quality or access.

- These opportunities could also result in non-financial benefits such as improved healthcare quality, increased access, better patient experience, and greater clinician satisfaction.

- As our case studies highlight, both the challenges to adoption and actionable solutions are becoming better understood as more organizations pilot AI.

- Recent market trends also suggest that AI in healthcare may be at a tipping point.

Still, taking full advantage of the savings opportunity will require the deployment of many AI-enabled use cases across multiple domains.

Ongoing research and validation of these use cases is needed.

- This could include conducting randomized control trials to prove the impact of AI in clinical domains to increase confidence for broader deployment.

- However, given that these studies will likely require a long timeline, additional work focused on case studies of successful deployments may provide greater evidence for organizations to overcome internal inertia in the near term.

- Finally, an independent third party could create a central data repository of AI deployments — both successful and unsuccessful — which would allow for more robust econometric analyses to inform rapid scaling.

As other industries have shown, AI as a technology could have an outsized financial and non-financial impact in healthcare, enabling patients to receive better care at a lower cost.

The next few years will determine whether this promise becomes a reality.

INFOGRAPHIC

Figure 6. Breakdown of overall AI net savings opportunity within next five years using today’s technology without sacrificing quality or access

Figure 2. Hospital AI domains and example use cases

Figure 3. Physician group AI domains and example use cases

Figure 4. Private payer AI domains and example use cases

ORIGINAL PUBLICATION [full version]

Can artificial intelligence (AI) improve productivity in healthcare? That is a central question in the United States and the focus of this paper.

In the United States, healthcare is considered too expensive for what it delivers. Businesses are looking to manage their costs, and healthcare spending is a large and growing expense.

As healthcare spending grows in the public sector, it crowds out other governmental budget priorities.

Previous research has found that healthcare in the United States could be more productive — both costing less and delivering better care (Berwick et al., 2012[1]; Sahni et al., 2019[2]). AI is likely to be part of the solution.

The improvement in US healthcare productivity could manifest in several ways.

Reducing administrative costs is one example. Administrative costs are estimated to account for nearly 25 percent of all US healthcare spending (Sahni et al., 2021)[3]; AI could reduce this burden. Harnessing clinical knowledge to improve patient health is a second way. Medical knowledge is growing so rapidly that only 6 percent of what the average new physician is taught at medical school today will be relevant in ten years (Rajkomar et al., 2019)[4]. Technology such as AI could provide valuable clinical data to the clinician at the time of diagnosis. Improving clinical operations is still another example. Operating rooms (ORs) are one of hospitals’ most critical assets. Yet inefficient operations can result in wasted hours, leading to excessive building of space, hindering patient access, degrading the patient experience, and reducing hospitals’ financial margins.

In this paper we focus on two questions about AI.

1.First, how much might be saved by wider adoption of AI in healthcare?

To answer this, we estimate potential savings by considering how AI might affect processes for three stakeholder groups — hospitals, physician groups, and private payers.

For each stakeholder group, we illustrate AI-enabled use cases across both medical and administrative costs and review case studies.

Using national healthcare spending data, we then scale the estimates to the entire US healthcare industry.

We find that AI adoption within the next five years using today’s technologies could result in savings of 5 to 10 percent of healthcare spending, or $200 billion to $360 billion annually in 2019 dollars, without sacrificing quality and access.[5]

For hospitals, the savings come largely from use cases that improve clinical operations (for example, operating room optimization) and quality and safety (for example, condition deterioration management or adverse event detection).

For physician groups, the savings also mostly come from use cases that improve clinical operations (for example, capacity management) and continuity of care (for example, referral management).

For private payers, the savings come largely from use cases that improve claims management (for example, auto-adjudication or prior authorization), healthcare management (for example, tailored care management or avoidable readmissions), and provider relationship management (for example, network design or provider directory management).

While we only quantify cost savings in this paper, there are additional non-financial benefits from the adoption of AI, including improved healthcare quality, increased access, better patient experience, and greater clinician satisfaction.

The magnitude of these savings raises a second question: if AI in healthcare can be so valuable, why is it not in greater use?

At the organizational level, in our experience, there are six factors for successful AI adoption.

AI’s limited uptake can be partly explained by the difficulty of addressing these factors, such as the failure to create “digital trust” with patients.

In addition, we discuss industry-level challenges such as data heterogeneity, lack of patient confidence, and misaligned incentives.

Recent market trends, such as increasing venture capital and private equity investments, may increase the rate of AI adoption in the near future.

The paper is organized as follows.

- Section I outlines the scope of potential uses of AI in healthcare.

- Section II lays out how AI might be used for the three specific stakeholder groups — hospitals, physician groups, and private payers — and presents case studies as examples.

- Section III estimates the annual net savings that might result from adopting AI across all of US healthcare.

- Section IV considers the challenges to greater adoption of AI, and

- Section V discusses how market trends may change the decisions that organizations make about adopting AI.

- The final section offers concluding thoughts.

We note that the authors of this paper are an unusual group compared with the authors of other economics papers. One of the authors is an academic, and three are consultants with extensive experience in healthcare.

Thus, our insights draw upon a combination of academic and industry experience.

In many cases, the insights are not based on randomized control trials or quasi-experimental evidence; rather, they are distillations of observations from a number of organizations, in and out of healthcare.

Given this, the reader should understand that the evidence base underpinning some of our conclusions is less analytically rigorous than traditional economics papers.

SECTION I. THE SCOPE OF AI

We define AI as a machine or computing platform capable of making intelligent decisions. Healthcare has more often pursued two types of AI: machine learning (ML), which involves computational techniques that learn from examples rather than operating from predefined rules; and natural language processing (NLP), which is a computer’s ability to understand human language and transform unstructured text into machine-readable structured data. An example of ML is recommending additional purchases based on a consumer’s current choices, such as a book or a shirt; an example of NLP is analyzing written customer feedback to identify trends in sentiment that can inform improvements in a product’s features.

It is not hard to envision the application of these technologies to healthcare. ML examples include predicting whether a patient is likely to be readmitted to a hospital; using remote patient monitoring to predict whether a patient’s condition may deteriorate; optimizing clinician staffing levels in a hospital to match patient demand; and assisting in interpreting images and scans. NLP examples include extracting words from clinician notes to complete a chart or assign codes; translating a clinician’s spoken words into notes; filling the role of a virtual assistant to communicate with a patient, help them check their symptoms, and direct them to the right channel such as a telemedicine visit or a phone call; and analyzing calls to route members to the right resource and to identify the most common call inquiries. Sometimes combining ML and NLP can create greater value; for example, using NLP to extract clinician notes and then using ML to predict whether a prior authorization is needed.

In general, AI-enabled use cases address operational processes. One type of operational change is simplifying an existing process. In these situations, the ideal processes usually are repetitive in nature, are highly manual, or involve complex decision trees. For example, forecasting inventory, demand, and capacity in the manufacturing, retail, and hospitality industries was once a highly manual job, involving meticulous note-taking and trend forecasts. AI can perform the same processes faster with more precision. Another type of operational change is the creation of new processes. These generally were not accessible to organizations until now, but AI has unlocked them. For example, some insurance companies allow customers to send a photo of an incident to initiate a claim, which is then automatically processed by AI.

The application of AI in these use cases allows value to be created in several ways. Labor productivity improvement is one of the most important levers in healthcare. Historically, labor productivity growth in healthcare has been negative; only education has performed worse among all US services industries over the past few decades (Sahni et al., 2019)[6]. For many healthcare organizations, labor represents the single largest variable-cost item. Value can also be created in non-financial ways. For example, furnishing clinicians with data at the point of service could improve the course of treatment selected for the patient based on clinical evidence. As a result, health outcomes may improve with no increase — or even a reduction — in costs.

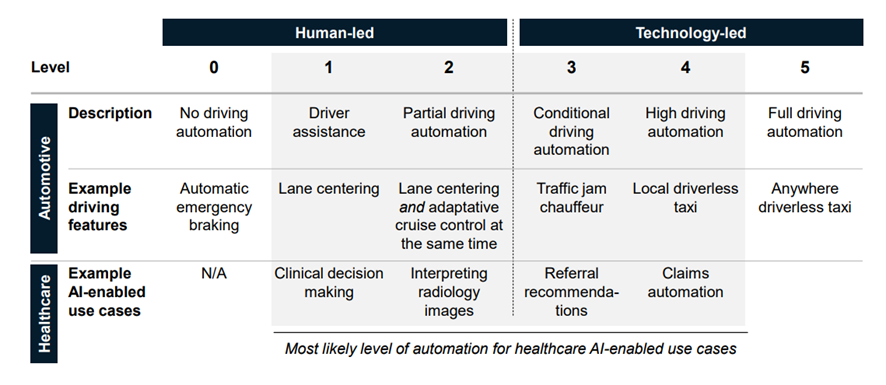

Figure 1. Society of Automotive Engineers levels of automation adapted to healthcare

Source: Society of Automotive Engineers; authors’ analysis

Adopting AI to create this value would unlock multiple levels of potential automation in healthcare. We illustrate these by considering the current use of AI in autonomous cars (Figure 1). The Society of Automotive Engineers defines five levels of automation (Society of Automotive Engineers, 2021)[7]. Each increasing level involves a greater degree of autonomous input: no driving automation but automatic emergency procedures in level 0; driver assistance such as lane centering in level 1; partial automation such as adaptive cruise control in level 2; conditional driving automation such as in traffic jams in level 3; local driverless taxis in level 4; and anywhere driverless taxis in level 5. At level 3 and above, the technology is in greater control than the human.

It is difficult to align on a single level for all of healthcare because AI-enabled use cases may vary. For example, clinical decision making is likely to approach level 1: the clinician makes final decisions jointly with the patient, but AI acts as a “member of the team” to present possible courses of treatments. The interpretation of radiology images could exemplify level 2, with AI reviewing an MRI or X-ray and outputting an interpretation. Humans would make the final decision for quality control and ensure the AI algorithm is trained properly. AI-enabled use cases in which technology would play the leading role could include referral recommendations (level 3) and claims automation (level 4).

SECTION II. DOMAINS OF AI IN HEALTHCARE

To understand how AI might influence healthcare spending, we start by breaking down the industry into five stakeholder groups — hospitals, physician groups, private payers, public payers, and other sites of care, such as dentists and home health.[8] We focus primarily on the first three, which collectively represent 80 percent of total industry revenue (Singhal et al., 2022)[9].

For each of these stakeholder groups, we identify the key domains with underlying AI-enabled use cases. A “domain” is defined as a core functional focus area for an organization. A “use case” is a discrete process that is addressed within a domain. For example, hospitals have clinical operations teams (a domain) that specialize in operating room efficiency (a use case). For each domain, we consider whether the use of AI will affect medical or administrative costs. We also note the position of each domain along the adoption curve. We define this as a typical technology S-curve — first developing solutions, then piloting, followed by scaling and adapting, and finally reaching maturity. In addition, we identify whether the processes affected are existing or new.

In addition, we provide a measure of impact on “total mission value.” Healthcare involves many non-financial factors, such as quality outcomes, patient safety, patient experience, clinician experience, and access to care. The combination of financial and non-financial factors is what we term total mission value.

A. HOSPITALS

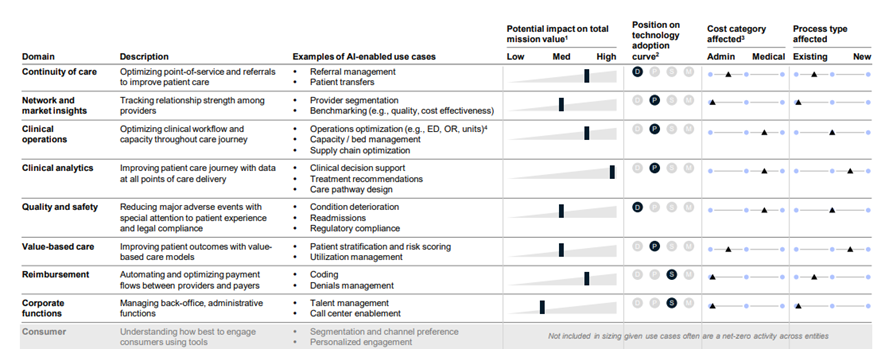

Domain breakdown. In our experience, AI-enabled use cases are emerging in nine domains: continuity of care, network and market insights, clinical operations, clinical analytics, quality and safety, value-based care, reimbursement, corporate functions, and consumer (Figure 2).[10] Within clinical operations, for example, hospitals are focusing on use cases such as improving the capacity of the operating room, freeing up clinical staff time, and optimizing the supply chain (Luo et al., 2020[11]; Kilic et al., 2020[12]). Clinical analytics, with AI-enabled use cases such as clinical decision making or treatment recommendations, is another area of focus for hospitals, usually within specialties such as radiology (Allen et al., 2021)[13]. A key domain, and the focus of much academic research, is quality and safety. This includes AI-enabled use cases such as predicting the likelihood of condition deterioration, an adverse event, or a readmission (Bates et al., 2021)[14].

Figure 2. Hospital AI domains and example use cases

1 We define “total mission value” as the combination of financial and non-financial factors, such as quality outcomes, patient safety, patient experience, clinician experience, and access to care

2 D = development of solutions; P = piloting; S = scaling and adapting; M = mature

3 Positioning represents the direct cost category affected; second order effects may also reduce costs, but are not estimated

4 ED = emergency department; OR = operating room

Source: Authors’ analysis

Some domains, such as reimbursement and corporate functions, are more advanced in AI adoption than others. Key reasons for the variation in uptake among hospitals include organizational priority and need, availability of data, and the share of AI deployment in the total budget.

Consider the quality and safety domain. There have been only a few successful use cases, such as identifying sepsis early or the prediction of adverse events (Bates et al., 2021[15]; Nemati et al., 2018[16]; Cooley-Rieders et al., 2021[17]). This is due in part to the need for a strong business case to launch a pilot. When an organization considers only financial factors, AI-enabled use cases usually do not meet the threshold for investment. The business cases for adopting AI become more compelling when the focus shifts to total mission value, which includes non-financial factors such as experience and access.

Five domains have a greater impact on administrative costs than on medical costs:

- continuity of care,

- network and market insights,

- value-based care,

- reimbursement, and

- corporate functions.

These are further along in part because administrative costs are generally associated with processes that that are manual and repetitive, which AI is well suited to address.

However, the overall opportunity is likely lower given that administrative costs represent a smaller portion of the total than medical costs do.

Case study in corporate functions. During the COVID-19 pandemic, one multi-state hospital’s call center experienced a large increase in call volumes as patients sought more information on topics such as billing, COVID-19 tests, COVID-19 vaccines, scheduling and finding a clinician, searching for care, and getting a telemedicine visit. The hospital had not anticipated the increase in call volumes and was not staffed accordingly; nor did it have adequate existing call routing protocols. As a result, the hospital observed higher call wait times and dropped calls, both of which negatively affected patient experience and access to care.

Using NLP, which is well suited for tasks that have a consistent set of outcomes, the hospital created a virtual agent (a digital version of a customer service representative) for its mobile app and website. This virtual agent would answer common questions and route patient questions to a specific, prebuilt process with the appropriate supporting information. As a result of this rollout, call volume decreased by nearly 30 percent, the patient experience improved, and managers redeployed workers to less manual, more customized tasks such as answering calls related to upcoming and completed procedures.

Case study in clinical operations. One large regional hospital was losing surgical volumes to other local hospitals. The surgical team investigated the operating room (OR) schedule and found that while ORs appeared to be 100 percent blocked, actual utilization was about 60 percent. Reasons for this underuse included historical block-scheduling techniques that did not adjust time allocation based on surgeon demand, scheduled time slot durations that did not reflect actual surgical times (for example, some operations were scheduled for longer than they actually took, leaving unused time), and manual processes related to the release and reallocation of unused blocks.

Hospital leadership and frontline managers used AI to optimize the OR block scheduler — the system for assigning surgical time slots to surgeons — for more than 25 ORs and dozens of surgeons. An AI algorithm ingested historical block utilization and trends; forecast case hours by specialty, physician group, or surgeon; and rules related to procedural equipment needs, staffing, and surgeon availability. An optimization algorithm was then run to generate proposed schedules for a given week, using current schedules as a reference. To ensure acceptance of the results, the hospital worked with surgeons throughout the process, incorporating their insights into the algorithms. The solution has increased the amount of open time in the OR schedule by 30 percent, making it easier to treat patients with critical needs sooner. To sustain this progress, a data scientist was assigned responsibility for the algorithm and provides ongoing review of the output with the OR team for continued buy-in.

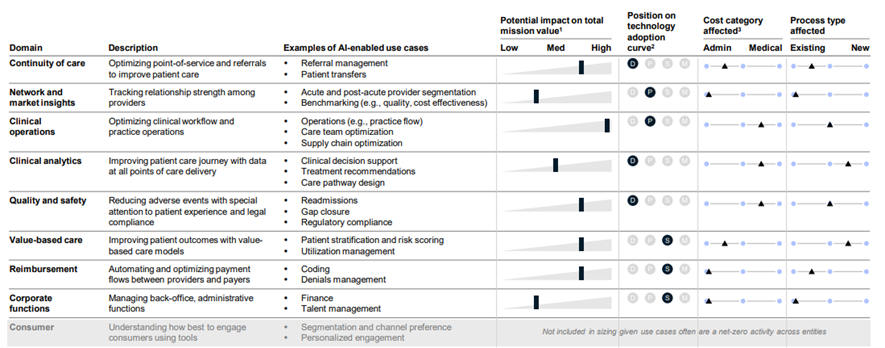

B. PHYSICIAN GROUPS

Figure 3. Physician group AI domains and example use cases

1 We define “total mission value” as the combination of financial and non-financial factors, such as quality outcomes, patient safety, patient experience, clinician experience, and access to care

2 D = development of solutions; P = piloting; S = scaling and adapting; M = mature

3 Positioning represents the direct cost category affected; second order effects may also reduce costs, but are not estimated

Source: Authors’ analysis

Domain breakdown. For physician groups, AI-enabled use cases are developing in the same nine domains as hospitals (Figure 3). Within clinical operations, physician groups aim to reduce missed visits (patients failing to show up for a planned appointment) and ensure access to procedures by focusing on overall workflow, operations, access, and care team deployment. For example, understanding which patients might miss an appointment or need support with transportation influences how the clinical team conducts outreach to patients and the overall schedule of the physician group. Quality and safety is another domain of focus, especially for physician groups in value-based arrangements, where quality and safety outcomes directly affect financial performance. For example, AI supporting a value-based arrangement may predict which patients are at higher risk for readmission, therefore enabling care team members to intervene and address a patient’s care needs to prevent deterioration in the condition. As these payment models grow in acceptance, particularly in primary care, physician groups are increasingly focusing on overall population health management use cases within the value-based care domain.

In terms of AI adoption, some domains are more mature than others. Those further along reflect the impact of market forces on physician group economics and the transition to value-based arrangements. For example, the clinical operations domain is more mature, given how central it is to a physician group’s economics, patient access, and patient and clinician experience. In contrast, continuity of care, an important aspect of care management, is less mature given the fragmented nature of data across providers. However, new interoperability application programming interfaces (APIs), which enable the exchange of data between two organizations — such as two providers or a payer and a provider — are making it easier to exchange data in standard formats.

As with hospitals, five of the domains have a greater impact on administrative costs than on medical costs: continuity of care, network and market insights, value-based care, reimbursement, and corporate functions. These five domains are generally further along the adoption curve but likely have smaller total impact. Further, AI-enabled use cases in these domains tend to address existing processes. Future adoption in these domains is tied to market trends — such as the growth of value-based arrangements mentioned above — and the increase in vendors who can serve physician groups.

Case study in value-based care. One large physician group was in a value-based arrangement for a single chronic disease and searching for innovative ways to manage the total cost of care while improving outcomes for its patients. To meet those goals, the organization identified reducing preventable complications as an opportunity area. The organization observed that about 10 percent of patients were admitted to the hospital on a monthly basis. Using AI, the physician group developed a risk model to assess likelihood of unplanned admission. The AI application ingested data from several sources (for example, electronic health records, lab results, demographics, risk scores, and health information exchange admission, discharge, and transfer feeds) to develop the model and understand the main variables influencing unplanned admission. The initial model showed a potential decrease of several percentage points in inpatient spending due to better care management. The physician group is now planning to deploy the algorithm more broadly based on the prototype models. As a result, members of the care team will be able to better prioritize their outreach to patients, more efficiently using their time to improve patient outcomes. To operationalize this, the physician group is creating new clinical workflows that are helping the care team better focus their attention and resources.

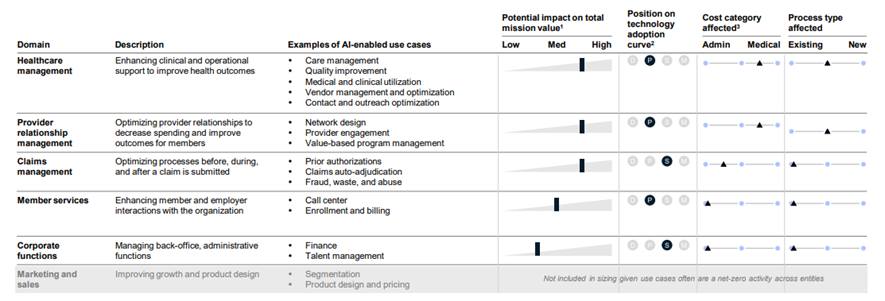

C. PRIVATE PAYERS

Domain breakdown. In our experience, AI-enabled use cases are emerging in six domains for private payers: healthcare management, provider relationship management, claims management, member services, corporate functions, and marketing and sales (Figure 4).[18] Within healthcare management, private payers are focusing on care management, medical and clinical utilization and spending, and quality AI-enabled use cases. For example, private payers are attempting to predict behavioral health needs to better match patients with support resources and seeking to improve care management programs that help prevent avoidable readmissions. Another example is claims management, where private payers are using AI to improve auto-adjudication rates; predict and improve prior authorization outcomes to enable greater access to care; and prevent fraud, waste, and abuse. Further, the provider relationship management domain focuses on designing networks that enable better quality outcomes and access in a cost-effective way for members.

Figure 4. Private payer AI domains and example use cases

1 We define “total mission value” as the combination of financial and non-financial factors, such as quality outcomes, patient safety, patient experience, clinician experience, and access to care

2 D = development of solutions; P = piloting; S = scaling and adapting; M = mature

3 Positioning represents the direct cost category affected; second-order effects may also reduce costs, but are not estimated

Source: Authors’ analysis

Adoption of AI varies across these domains. Claims management and corporate functions generally are more mature in their adoption of AI. Many use cases, such as processing a prior authorization or adjudicating a claim, are largely repetitive processes that are best suited for AI.

Three domains have more impact on administrative costs than on medical costs: claims management, member services, and corporate functions. The opportunity in these domains is substantial but less than for medical costs, given administrative costs are a smaller portion of total costs. For the domains that are focused on medical cost, there are also large non-financial opportunities, including improving health, quality, and member experience. In general, use cases tend to be focused on existing processes across all domains.

Case study in claims management. One large private payer, experiencing high costs and conducting an overall effort to improve its financial position, assessed areas for improvement in claims management. The analysis concluded that the organization could replace existing manual processes with AI to address fraud, waste, and abuse (FWA) among providers. As a result, a team built an AI classification model to identify potential FWA based on prior patterns observed in several years of claims data. The output of the model was a list of providers for further investigation. The team could then manually validate the list and determine next steps. This AI-enabled identification model allowed the payer to streamline operations and inform efforts that resulted in the reduction of medical costs by about 50 basis points. The payer’s FWA team maintains the AI model on an ongoing basis.

Case study in healthcare management. To improve patient outcomes, a private payer focused on how to reduce the readmissions rate for its most vulnerable members. To address these readmissions, the organization developed an ML model that ingested a variety of claims and member demographic information. The output identified which patients were most likely to have a readmission, quantify the differences between these patients and those who did not have a readmission, and understand which parts of the care journey were linked to the readmission. The private payer then used the output to inform core business processes such as care management outreach. For example, the organization created a specialized outreach team of care managers who used the output to prioritize tactics for these vulnerable patients. As a result of this ML model and associated personalized-marketing techniques, about 70 percent more members connected with their care managers compared with previous efforts that did not use the model. Follow-up visits with primary care physicians within 30 days of discharge increased by about 40 percent, and the all-cause readmission rate decreased by about 55 percent for this cohort.

SECTION III: OPPORTUNITY SIZE

Based on the domains discussed above, we have estimated the annual net savings that AI could create for US healthcare in the next five years. Net savings is defined as total gross savings less annual expenses to operate AI. We derive the savings estimates for each domain from our experience working with healthcare organizations; there are few experimental studies of the impact of AI on costs or outcomes to inform our analysis. All savings estimates are based on the use of technologies available today and assume that adoption reaches full scale.

To estimate the total AI opportunity, we first estimate the revenue for each stakeholder group from 2019 National Health Expenditure data. Using McKinsey’s proprietary value pool data, we subtract each stakeholder group’s total earnings before interest and taxes (EBIT), leaving total costs. For hospitals and physician groups, we estimate three cost categories: administrative costs, medical costs associated with labor (for example, clinicians), and non-labor medical costs (for example, diagnostics and supplies). For private payers, we estimate two cost categories: administrative costs and medical costs.

With this baseline, each AI domain described in Section II is then aligned to a cost category. Based on our experience, we estimate a gross savings percentage for each domain. We break down what portion of these savings will affect administrative or medical costs. One key adjustment is converting gross savings to net savings. This conversion represents the expense needed to maintain AI. Based on our experience, we model labor and technology maintenance expenses for each stakeholder group. The total amount is then subtracted from gross savings to estimate a net savings range.

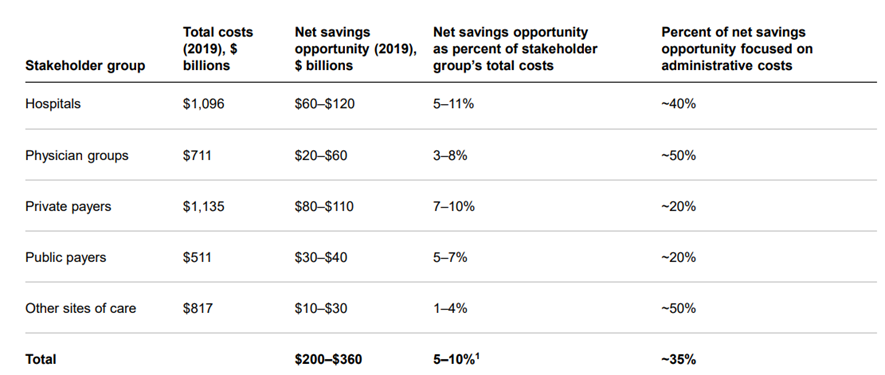

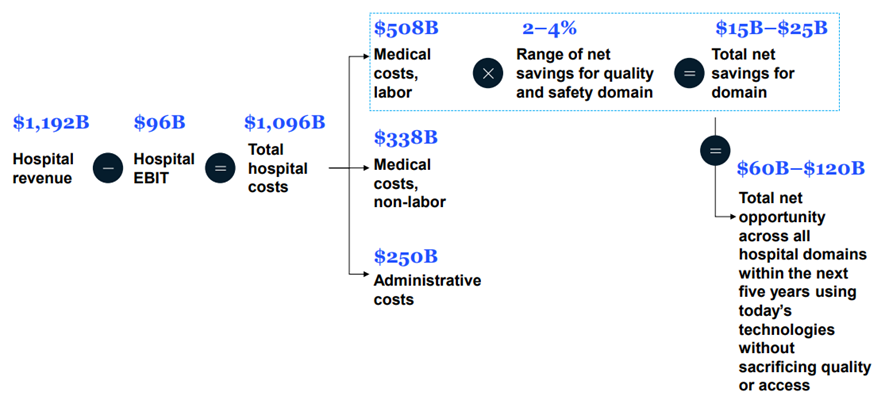

We then multiply these percentages by the dollar values in each cost category to estimate a net savings value for each domain. Summing the estimated savings for each domain results in the total net savings opportunity for a stakeholder group. Figure 5 shows an example of the quality and safety domain for hospitals. We begin with total hospital revenue as reported in the National Health Expenditure data of $1,192 billion in 2019. We subtract hospital EBIT to estimate a total for hospital costs. Total hospital costs are then broken into three cost categories. The quality and safety domain largely affects labor within medical costs, which we estimate to be $508 billion in 2019. Using the net savings rate for this domain (after accounting for the gross-to-net conversion), total net savings is $15 billion to $25 billion. Repeating this for all the domains, we estimate a total annual net savings opportunity for hospitals of $60 billion to $120 billion within the next five years using today’s technologies without sacrificing quality or access.

Figure 5. Example of a hospital domain calculation: Quality and safety

Note: All data in 2019 dollars

Source: National Health Expenditures data; authors’ analysis

To consider the full AI opportunity in healthcare, we also include public payers and other sites of care such as dentists and home health. For public payers, we begin with the AI opportunity estimated for private payers, which have several similar functions and operations. Referencing previous research, we estimate the total costs to be about 45 percent of those for private payers (Sahni et al., 2021)[19]. We further assume the savings opportunity would be about three-quarters that of private payers given that public payers do not undertake all the same functions to the same extent, such as provider relationship management and healthcare management. For other sites of care, we begin with the AI opportunity estimate for physician groups. Similarly referencing previous research, we estimate the total costs to be about 115 percent of those for physician groups (Sahni et al., 2021)[20]. We further assume the savings opportunity would be about half that of physician groups given differences in patient acuity, clinical staff mix (for example, less clinician time per clinical episode), and fewer applicable AI domains.

Our estimates do not include one-time implementation costs, which in our experience are 1.0 to 1.5 times the annual net savings. One-time implementation costs relate directly to building an AI-enabled use case, which includes hiring specialized talent, creating incremental infrastructure or computing power, and aggregating and cleaning the necessary data. One-time implementation costs do not include large investments such as new underlying core technology or last-mile change management, both of which could be necessary and can vary greatly by organization.

A. HOSPITALS

In 2019 dollars, total costs for hospitals are about $1,096 billion, of which 80 percent is medical and 20 percent is administrative. With about 6,000 hospitals nationally, this is a fragmented market. The top 10 hospital systems accounted for about 18 percent of admissions in 2017 (Sahni et al., 2019)[21]. Types of facilities include community hospitals and academic medical centers. The typical hospital has an “all-payer margin” of about 6 to 7 percent (Medicare Payment Advisory Commission, 2022)[22].

Based on our calculations, hospitals employing AI-enabled use cases could achieve total annual run-rate net savings of $60 billion to $120 billion (roughly 4 to 10 percent of total costs for hospitals) within the next five years using today’s technologies without sacrificing quality or access. Clinical operations — encompassing emergency room and inpatient care, capacity and workflow, diagnostics, supply chain, and clinical workforce management — and quality and safety are the primary drivers of this opportunity. About 40 percent of total savings would come from reducing administrative costs (roughly 9 to 19 percent of this cost category), with the remaining 60 percent from reducing medical costs (roughly 4 to 8 percent of this cost category). About 45 percent of total savings would come from simplifying existing processes, with the remaining 55 percent from creating new processes.

B. PHYSICIAN GROUPS

In 2019 dollars, total costs for physician groups are about $711 billion, of which 70 percent is medical and 30 percent administrative. The physician group landscape is fragmented, with about 125,000 groups nationally, including those employed by hospitals, owned by private organizations, or independent (Sahni et al., 2021)[23].

Based on our calculations, physician groups employing AI-enabled use cases could achieve total annual run-rate net savings of $20 billion to $60 billion (roughly 3 to 8 percent of total costs for physician groups) within the next five years using today’s technologies without sacrificing quality or access. The main domain of opportunity, similar to hospitals, is clinical operations, with a focus on outpatient operations and access, supply chain, and clinical workforce management. About 50 percent of total savings would come from reducing administrative costs (roughly 4 to 14 percent of this cost category), with the remaining 50 percent from reducing medical costs (roughly 2 to 6 percent of this cost category). About 45 percent of total savings would come from simplifying existing processes, with the remaining 55 percent from creating new processes.

C. PRIVATE PAYERS

In 2019 dollars, total costs for private payers are about $1,135 billion, of which 85 percent is medical and 15 percent administrative. In 2017, the top five private payers plus Medicare (Part A/B only) and Medicaid (fee-for-service only) accounted for about 58 percent of covered lives, and the 350-plus other private payers covered the remaining 42 percent (Sahni et al., 2019)[24]. Types of private payers include national, regional, and local for-profit and not-for-profit organizations.

Based on our calculations, private payers could achieve total annual run-rate net savings of $80 billion to $110 billion (roughly 7 to 9 percent of total costs for private payers) within the next five years using today’s technologies without sacrificing quality or access. The primary domains of opportunity are healthcare management (including care management and avoidable readmissions), claims management (including FWA identification, prior authorizations, and adjudication), and provider relationship management (including network design, value-based care, and provider directory management). About 20 percent of total savings would come from reducing administrative costs (roughly 8 to 14 percent of this cost category), with the remaining 80 percent from reducing medical costs (roughly 6 to 9 percent of this cost category). About 55 percent of total savings would come from simplifying existing processes, with the remaining 45 percent from creating new processes.

D. OVERALL

With these estimates, we then scale the savings to the entire US healthcare industry (Figure 6). In 2019 dollars, we estimate the annual run-rate net savings to be $200 billion to $360 billion within the next five years using today’s technologies without sacrificing quality or access. This would amount to a 5 to 10 percent overall reduction in US healthcare spending. AI adoption could also create non-financial benefits such as improved healthcare quality, increased access, better patient experience, and greater clinician satisfaction. (In this paper, we do not offer an estimate of these non-financial benefits.)

Figure 6. Breakdown of overall AI net savings opportunity within next five years using today’s technology without sacrificing quality or access

1 This represents the percent of total national health spending in 2019.

Source: National Health Expenditures data; authors’ analysis

Administrative costs could be reduced by 7 to 14 percent, roughly $65 billion to $135 billion annually. This is about 35 percent of total savings. The remaining 65 percent could reduce medical costs by 5 to 8 percent, roughly $130 billion to $235 billion annually. The overall AI opportunity is divided nearly equally between simplifying existing processes and creating new processes.

SECTION IV. ADOPTION CHALLENGES

Despite the large opportunity, the AI adoption rate in healthcare has lagged behind that in other industries (Cam et al., 2019)[25]. Generally, technology adoption follows an S-curve — first developing solutions, then piloting, followed by scaling and adapting, and finally reaching maturity. Other industries have already reached the final stage of the S-curve; for example, financial services companies deploy sophisticated AI algorithms for fraud detection, credit assessments, and customer acquisition. Mining companies use AI to boost output, reduce costs, and manage the environmental impact of new projects. Retailers use AI to predict which goods will interest a customer based on the customer’s shopping history.

Across nearly all the domains identified in Section II, AI adoption in healthcare is at an earlier stage of the S-curve. There are several possible reasons for this. Many economists believe that AI is underused because the healthcare payment system does not provide incentives for this type of innovation. Another view is that management barriers, both at the organizational and industry level, are responsible for slower adoption in healthcare.

In this paper, we do not settle the debate about whether better incentives will lead to greater adoption of AI. Rather, we discuss the managerial difficulties in bringing AI to bear in healthcare. Even if the right payment models were in place, organizations would still need to overcome challenges such as legacy technology, siloed data, nascent operating models, misaligned incentives, industry fragmentation, and talent attraction (Goldfarb et al., 2022[26]; Henke et al., 2016[27]).

In our experience, private payers are further along the AI adoption curve than other healthcare organizations, although larger national private payers with greater resources are more advanced in their use of AI compared with smaller regional private payers that may face resource and talent attraction challenges. Hospitals have piloted AI and are beginning to scale adoption in some domains, with larger hospitals having done more than smaller hospitals. Most physician groups are at the beginning of their journey (unless employed by hospitals).

In this section, we discuss specifics about what is needed for AI adoption in healthcare. We break these down into “within” and “between / seismic” factors. “Within” factors are those that can be controlled and implemented by individual organizations. “Between” factors require collaboration between organizations but not broader, industry-wide change, and “seismic” factors require broad, structural collaboration across the US healthcare industry (Sahni et al., 2021)[28].

A. ‘WITHIN’ CHALLENGES

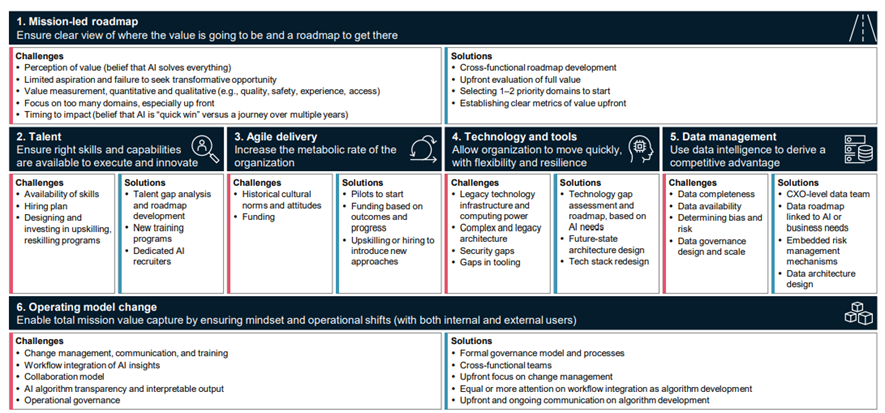

In our experience, successful AI adoption depends on six factors (Figure 7). These are the same for all organizations across industries, though some of the underlying challenges are specific to healthcare.

The first factor is a mission-led roadmap. The roadmap should offer a clear view of value, link to business objectives and mission, and be sequenced for implementation. A key challenge is ensuring the end state is a transformative view of the organization, not incremental. Each AI-enabled use case should be quantified, which presents additional hurdles for healthcare organizations because value extends into non-financial factors such as quality outcomes, patient safety, patient experience, clinician experience, and access to care. As noted above, we refer to this combination of financial and non-financial factors as total mission value. In our experience, the most successful organizations rely on strong collaboration between business and technology leaders to develop and implement this roadmap.

Figure 7. Factors for successful AI adoption with associated challenges and solutions within healthcare organizations

Source: Carey D, Charan R, Lamarre E, et al. The CEO’s Playbook for a Successful Digital Transformation. Harvard Business Review. 20 Dec 2021; Rajkomar A, Dean J, Kohane I. Machine Learning in Medicine. N Engl J Med 2019 Apr 4;380(14):1347–1358 2019;380:1347–1358; Bates DW, Auerbach A, Schulam P, et al. Reporting and Implementing Interventions Involving Machine Learning and Artificial Intelligence. Ann Intern Med 2020 Jun 2;172(11 Suppl):S137-S144; Shaw J, Rudzicz F, Jamieson T, Goldfarb A. Artificial Intelligence and the Implementation Challenge. J Med Internet Res 2019 Jul;21(7):e13659; Singh RP, Hom GL, Abramoff MD, Campbell JP, Chiang MF. Current Challenges and Barriers to Real-World Artificial Intelligence Adoption for the Healthcare System, Provider, and the Patient. Transl Vis Sci Technol 2020 Aug 11;9(2):45; He J, Baxter SL, Xu J, et al. The practical implementation of artificial intelligence technologies in medicine. Nat Med. 2019 Jan;25(1):30–36; Authors’ analysis

A second factor is talent. Organizations must ensure that the right skills and capabilities are available across the organization. Talent shortages are common, especially in AI (Zwetsloot et al., 2019)[29]. Many organizations have addressed these shortages by establishing talent hubs, sometimes in a different city with operations than headquarters, but many healthcare organizations face the additional challenge of being inherently local. Still, some are experimenting with ways to make this work — for example, by centralizing talent in a nearby location or using remote work options.

Agile delivery, or accelerating an organization’s decision-making and delivery processes, is a new approach for many healthcare organizations. Changing the culture to move away from historical processes and ways of working is a challenge for organizations in all industries. It is an especially large hurdle in healthcare, where culture is often more deeply rooted than in other industries, and where clinicians are justifiably concerned that the process of change might harm patients. In our experience, organizations that empower small, integrated agile teams are more likely to have successful AI deployments.

Enabling agile delivery requires technology and tools that are flexible, scalable, secure, and resilient. Organizations in all industries confront complex legacy IT environments. This is particularly true in healthcare given the relatively low levels of investment in technology and high levels of customization. In our experience, successful deployments generally overinvest in the enablers of AI, such as core technology architecture and data systems.

Data management, or the use of data to derive a competitive advantage, is often overlooked in AI deployments, though it is one of the most critical factors. Organizations in all industries face key challenges with data fragmentation and quality. The challenge is even greater in healthcare given the large number of systems, general lack of interoperability, and data privacy and usage requirements. In our experience, the most successful AI deployments establish a dedicated function to manage all data at the beginning of any adoption journey.

Finally, establishing the right operating model is key.[30] Such a model enables an organization to capture full mission value by encouraging mindset and operational shifts among both internal and external users. Determining the right operating model is difficult in any industry, and the number of stakeholders, need for change management with providers, and heightened attention to security and model risk increase the challenge in healthcare. In our experience, organizations that deploy more central structures to build capabilities, consistency, and rigor from the beginning position themselves for more successful AI deployments, while setting up the operating model to work closely with their business partners.

While it is critical for organizations to pursue all six factors, it is just as important to foster “digital trust” among individuals — to inspire confidence that the organization effectively protects data, uses AI responsibly, and provides transparency. Building this trust requires organizations to establish the right controls, processes, and risk management. Without digital trust and the responsible use of AI, healthcare organizations may experience greater scrutiny and a slower pace of use-case scaling.

Investing in addressing these challenges is critical. Across industries, the highest performers spent 30 to 60 percent more than others when adopting technologies such as AI and expect to increase their budgets 10 to 15 percent over the following year. Meanwhile, lesser performers report small or no increases (D’Silva et al., 2022)[31].

B. ‘BETWEEN’ AND ‘SEISMIC’ CHALLENGES

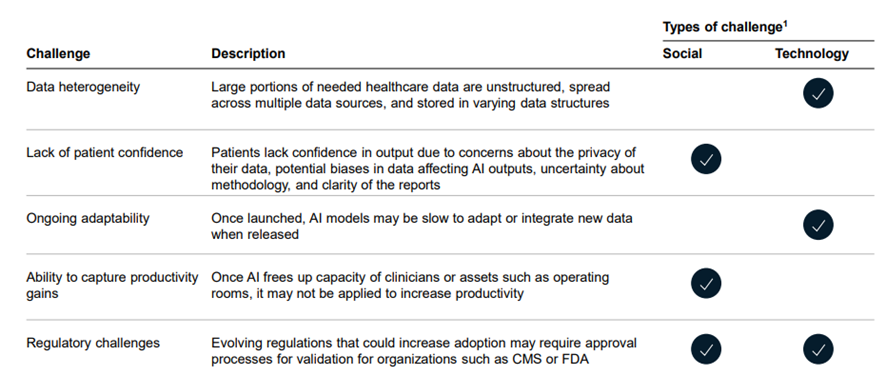

Even if a healthcare organization successfully deploys AI, it will face ongoing industry-level challenges — factors that are out of the organization’s control and can hinder widespread adoption. These include data heterogeneity, lack of patient confidence, ongoing adaptability, the ability to capture productivity gains, and regulatory challenges (Figure 8).

These industry-level challenges take two forms: social and technology. By social challenge, we mean one in which the industry would need to encourage stakeholders such as physicians to adopt the same approach, process, or standard. By technology challenge, we mean one in which the hurdle to adoption relates to the need for a technology solution.

Figure 8. Industry-level challenges by type

1 By social challenge, we mean one in which the industry would need to encourage stakeholders to adopt the same approach, process, or standard. By technology challenge, we mean one in which the hurdle to adoption relates to the need for a technology solution

Source: Authors’ analysis

Data heterogeneity in healthcare takes many forms. In industries with greater AI adoption, most data are structured. In healthcare, by contrast, large portions of key data are unstructured, existing in electronic health records (EHRs). Clinical notes, the clinician’s recording of a patient’s response to a particular treatment, are one example. Furthermore, these data exist in multiple sources, often with limited ways to connect disparate pieces of information for an individual patient (Kruse et al., 2016)[32].

Patient confidence in AI output is also critical to the integration of information into the clinical workflow. One issue is privacy. Patients may worry about how their data are being used and prevent the application of AI for their medical needs. Another concern is whether AI output can be trusted. There are many examples of biases in algorithms, and patients may not trust AI-generated information even if a clinician validates it. There are also methodological concerns such as validation and communication of uncertainty, as well as reporting difficulties such as explanations of assumptions (Bates et al., 2020[33]; Shaw et al., 2019[34]; Singh et al., 2020[35]; He et al., 2019[36]).

In addition, questions arise about whether AI-enabled use cases would cement certain biases in existing data and be slow to respond to new types of data. For example, an organization using AI to help define clinical treatment pathways might need to control for biases in existing treatment recommendations and determine how to remove them. In addition to adding AI ethics to model development, organizations are addressing bias by creating synthetic data — manufactured data designed to train a model on a certain set of inputs, similar to real-world data. Furthermore, as healthcare generates new data, these changes may require previously developed models to be refreshed.

Many clinicians and healthcare executives are optimistic that AI could address ongoing productivity challenges in healthcare. Historical analyses have shown negative labor productivity growth in healthcare and a likelihood that clinician shortages will continue (Sahni et al., 2019[37]; Berlin et al., 2022[38]). If adopted appropriately, AI could free up clinician capacity. The question arises, though, whether clinicians will use the excess capacity to see more patients or to complete non-clinical tasks.

Finally, in the United States, regulations generally focus on protecting the patient, given the private and sensitive nature of each person’s data. But regulation also plays other roles in AI. For example, Medicare and Medicaid are beginning to reimburse for AI applications, though adoption is still in the early stages. This is unique to healthcare; organizations in other industries have to pay for AI themselves. Validation that algorithms are clinically robust and safe is another issue. For example, the Food and Drug Administration (FDA) established standards for evaluating software as a medical device and AI-enabled medical devices. Dozens of AI products have since received approval, the majority in the past five years. Examples of digitally enabled therapeutics include those for treating type 2 diabetes and substance use disorder. This type of industry-level change could provide greater confidence for patients and clinicians using AI.

SECTION V. CHANGES THAT MAY IMPROVE AI ADOPTION

Based on our experience, fewer than 10 percent of healthcare organizations today fully integrate AI technologies into their business processes. But the benefits of doing so are meaningful: in our experience, organizations that deploy AI have twice the five-year revenue CAGR compared with others that do not. With a $200 billion to $360 billion opportunity in healthcare and such a small subset of organizations capturing the potential, what might the future hold? Will AI adoption accelerate?

Several trends suggest the tide may soon turn. First, the COVID-19 pandemic, coupled with rising inflation and labor shortages, is straining the finances of healthcare organizations (Singhal et al., 2022)[39]. For example, all seven of the largest publicly traded payers have announced productivity improvement programs in the past few years. Further, research shows that the most successful organizations coming out of a recession generally have run larger productivity improvement programs (Gorner et al., 2022)[40]. This could be a boon for the adoption of AI-enabled use cases — especially use cases that focus on administrative costs, which are usually passed over in favor of a focus on medical costs.

A second trend is the flow of investment into AI technologies, even in today’s uncertain macroeconomic climate. From 2014 to 2021, the overall number of venture capital–backed healthcare AI start-ups increased more than fivefold. Over the same period, the number of private equity deals for healthcare AI organizations increased more than threefold.

At the organizational level, there are indications that the C-suite’s appreciation for the potential of technologies like AI is growing. For example, nearly all of the top 15 private payers have a designated chief analytics or chief data officer. Dozens of hospitals do as well, including most of the largest in the United States. This elevation of business importance suggests that more AI deployments may be on the way.

At the industry level, evolving regulations may enable the creation of new data sets that feed AI. For example, recently introduced medical price transparency regulations promise to increase the availability of hospital and private payer data. Alone, these data may not be good enough for AI algorithms to generate insights; however, if coupled with other data sets, such as member or census data, they could accelerate the adoption of AI. In addition, the Centers for Medicare & Medicaid Services (CMS) has been developing interoperability rules and APIs that require data to be made available in a consistent structure to be exchanged across organizations.

SECTION VI. CONCLUSIONS

The promise of AI in healthcare has been a topic of discussion in the industry for more than a decade. But its potential has not been quantified systematically, and adoption has been lacking. We estimate that AI in healthcare offers a $200 billion to $360 billion annual run-rate net savings opportunity that can be achieved within the next five years using today’s technologies without sacrificing quality or access. These opportunities could also result in non-financial benefits such as improved healthcare quality, increased access, better patient experience, and greater clinician satisfaction. As our case studies highlight, both the challenges to adoption and actionable solutions are becoming better understood as more organizations pilot AI. Recent market trends also suggest that AI in healthcare may be at a tipping point.

Still, taking full advantage of the savings opportunity will require the deployment of many AI-enabled use cases across multiple domains. Ongoing research and validation of these use cases is needed. This could include conducting randomized control trials to prove the impact of AI in clinical domains to increase confidence for broader deployment. However, given that these studies will likely require a long timeline, additional work focused on case studies of successful deployments may provide greater evidence for organizations to overcome internal inertia in the near term. Finally, an independent third party could create a central data repository of AI deployments — both successful and unsuccessful — which would allow for more robust econometric analyses to inform rapid scaling.

As other industries have shown, AI as a technology could have an outsized financial and non-financial impact in healthcare, enabling patients to receive better care at a lower cost. The next few years will determine whether this promise becomes a reality.

REFERENCES

See the original publication

References

See original publication https://www.nber.org