This is an excerpt from “2022 Healthcare Provider IT Report — Post-Pandemic Investment Priorities”, published by Klas and Bain in October 2022.

Eric Berger, Laila Kassis , Aaron Feinberg , Michael Brookshire , John Day , Rebecca Hammond

October 2022

Competitive pressures in the provider software space show no signs of abating

Executive Summary:

Joaquim Cardoso MSc.

health systems transformation — center of excellence

October 22, 2022

xxx

Where spending is happening: Priority categories for the next year

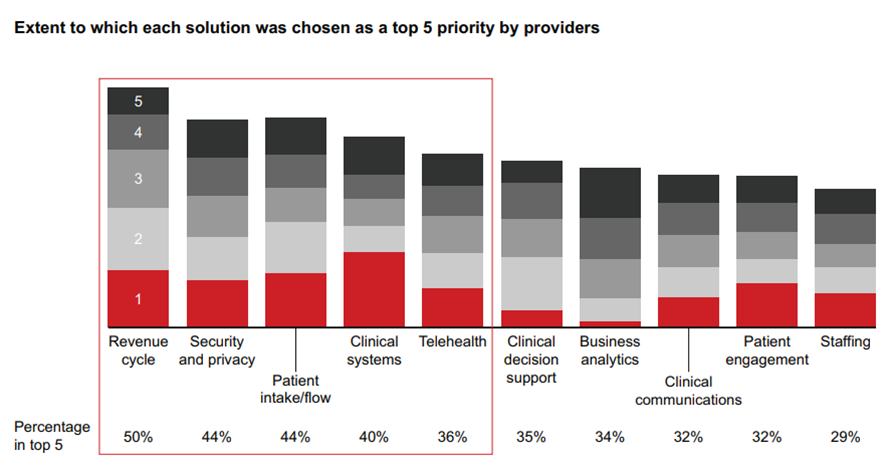

Providers cite revenue cycle management (RCM), security and privacy, patient intake/flow, clinical systems, and telehealth as the most strategically important categories for software investment over the next year (see Figure 4).

Infographic:

Figure 4: Top provider investment priorities over the next 12 months

Sources: Provider interviews; Bain-KLAS 2022 Provider Executive Survey (N=289)

- 1.Revenue cycle management

- 2.Security and privacy

- 3.Patient intake / Patient flow

- 4.Clinical systems

- 5.Telehealth

ORIGINAL PUBLICATION (excerpt)

1.Revenue cycle management

Revenue cycle management software is critical in the current environment given the direct link with cash collections as well as the labor-intensive nature of revenue cycle processes.

This is especially true for smaller provider organizations navigating complex payer landscapes and physician groups that lag health systems on the adoption of RCM software.

Large health systems also continue to make investments in RCM, however, via both business process outsourcing and adoption of enhanced RCM software modules (e.g., complex claims, artificial intelligence–enhanced features).

Providers of all types cited RCM as a top priority for the next year, pointing to a broad set of specific priorities, including revenue integrity, charge capture, and complex claims, and underscoring a robust set of RCM needs across the provider ecosystem.

Large health systems also continue to make investments in RCM, however, via both business process outsourcing and adoption of enhanced RCM software modules (e.g., complex claims, artificial intelligence–enhanced features).

Figure 4: Top provider investment priorities over the next 12 months

Sources: Provider interviews; Bain-KLAS 2022 Provider Executive Survey (N=289)

2.Security and privacy

Security and privacy software is another top investment priority for providers over the next year.

Even before Covid-19, providers were vulnerable to cyberattacks. But the risks have risen.

And as a result of the increase in the number of nodes in provider tech ecosystems, there’s been a surge in security breaches.

From 2018 to 2021, the number of data breaches reported by providers to the US Department of Health and Human Services’ Office for Civil Rights has nearly doubled for incidents impacting 500 or more medical records.

Additionally, provider data breaches are getting more expensive.

According to data from IBM, the average cost of a provider data breach has now surpassed $10 million, up nearly 40% since 2020.

Our research shows that regional health systems, freestanding hospitals, and mental health providers are especially focused on security and privacy investments, especially in areas such as cybersecurity, IoT security, and patient privacy monitoring.

…regional health systems, freestanding hospitals, and mental health providers are especially focused on security and privacy investments, — especially in areas such as (1) cybersecurity, (2) IoT security, and (3) patient privacy monitoring.

3.Patient intake/flow

Patient intake/flow software remains another critical area for investment. Covid-19 stretched hospital capacity to the max while also driving the need for enhanced virtual intake processes.

As a result, providers continue to invest in patient flow systems and are also investing heavily in patient intake management tools and patient portals.

Many providers are recognizing the importance of simplifying intake processes to accelerate cash collections and provide more seamless patient experiences in a world where patients increasingly expect to navigate the health system like consumers.

As a result, providers continue to invest in patient flow systems and are also investing heavily in patient intake management tools and patient portals.

Many providers are recognizing the importance of simplifying intake processes to accelerate cash collections and provide more seamless patient experiences in a world where patients increasingly expect to navigate the health system like consumers.

4.Clinical systems

Clinical systems remain a top investment priority, with providers citing EMRs as their primary investment area.

While a few providers are making first-time investments in EMR solutions, most are planning investments focused on optimizing existing EMR systems to streamline provider workflows and boost productivity, extending core EMR environments to recently acquired entities, or even switching EMR vendors altogether.

…most are planning investments focused on: (1) optimizing existing EMR systems to streamline provider workflows and boost productivity, (2) extending core EMR environments to recently acquired entities, or (3) even switching EMR vendors altogether.

5.Telehealth

Telehealth, while having declined in importance since the nadir of the Covid-19 pandemic, remains a critical strategic priority.

Large national health systems view telehealth systems as integral to care delivery and are looking to bolster existing video consultation/collaboration platforms and add enhanced telehealth capabilities.

Given the value of greater integration between care delivery platforms and EMRs, some large providers appear to be reconsidering the virtual care platforms offered by their EMRs.

This suggests that some large EMR players, particularly Epic, are improving telehealth platforms that were insufficient for providers during the early days of Covid-19.

Given the value of greater integration between care delivery platforms and EMRs, some large providers appear to be reconsidering the virtual care platforms offered by their EMRs.

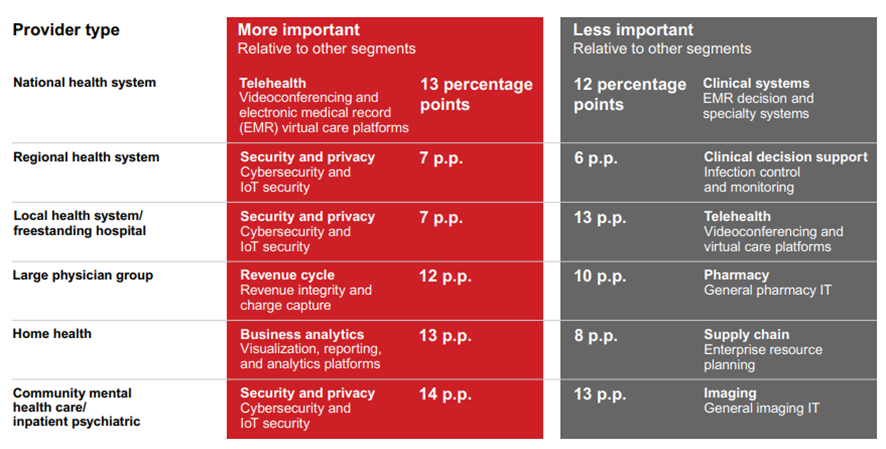

While each of these priorities is broadly relevant across a wide variety of organizations, certain priorities are uniquely important to different types of providers (see Figure 5).

Figure 5: Certain investment priorities are uniquely important to different provider types

Note: Percentage-point differences were calculated by comparing the percentage-point delta for provider type importance to the average importance across all other provider segments

Sources: Provider interviews; Bain-KLAS 2022 Provider Executive Survey (N=289)

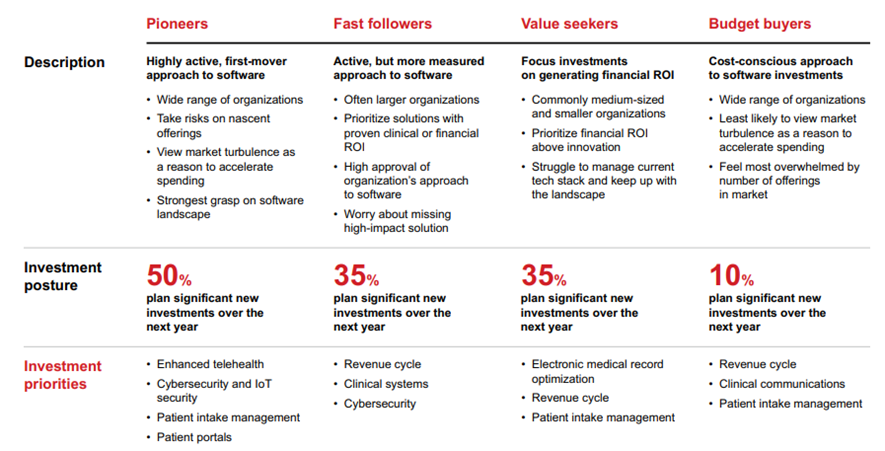

Figure 6: Provider software buyer archetypes based on organizational and behavioral characteristics

Note: Investment posture percentages for fast followers, value seekers, and budget buyers were rounded to the nearest 5 Sources: Provider interviews; Bain-KLAS 2022 Provider Executive Survey (N=289)

In addition, further nuances exist based on a broader matrix of provider organizational features and behavioral characteristics, which are critical for software vendors to consider when fine-tuning offerings and value propositions to meet the needs of customers.

Four provider archetypes emerged from our research based on their orientations toward making software investments (see Figure 6).