The State of Healthcare Report @ (HIMSS 21)

INDUSTRY INFOGRAPHIC

The State of Healthcare Report unveiled the disparities, challenges and opportunities of the healthcare industry and its stakeholders today. To gain such insight, HIMSS, along with its Trust partners-Accenture, The Chartis Group and ZS-surveyed more than 2,700 stakeholders, including patients, clinicians, health systems and payer organizations during March and April of 2021.

The report focuses on three main areas:

- digital health,

- financial health, and

- artificial intelligence (AI) and machine learning (ML).

Digital Health

In terms of digital health,

- most health systems have digital programs,

- but opportunities still exist to accelerate and expand -4% of health systems reported that they haven’t even begun to develop a digital presence yet.

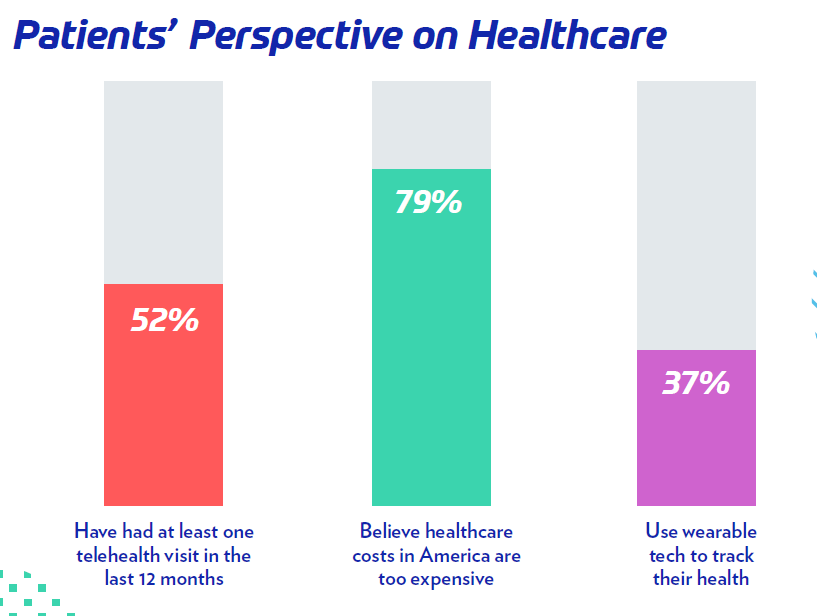

Clinicians largely agree that digital health tools are here to stay, as evidenced by the fact that 52% of patients have had at least one telehealth visit in the last 12 months.

Additionally, 64% of payers reported an accelerated adoption of digital health initiatives coming out of COVID-19.

Financial Health

When it comes to financial health,

- One in 10 clinicians (10%) see their practices in an unstable financial position.

- Conversely, 51% said their practices are “somewhat stable” and

- 19% said their practices are “highly stable.”

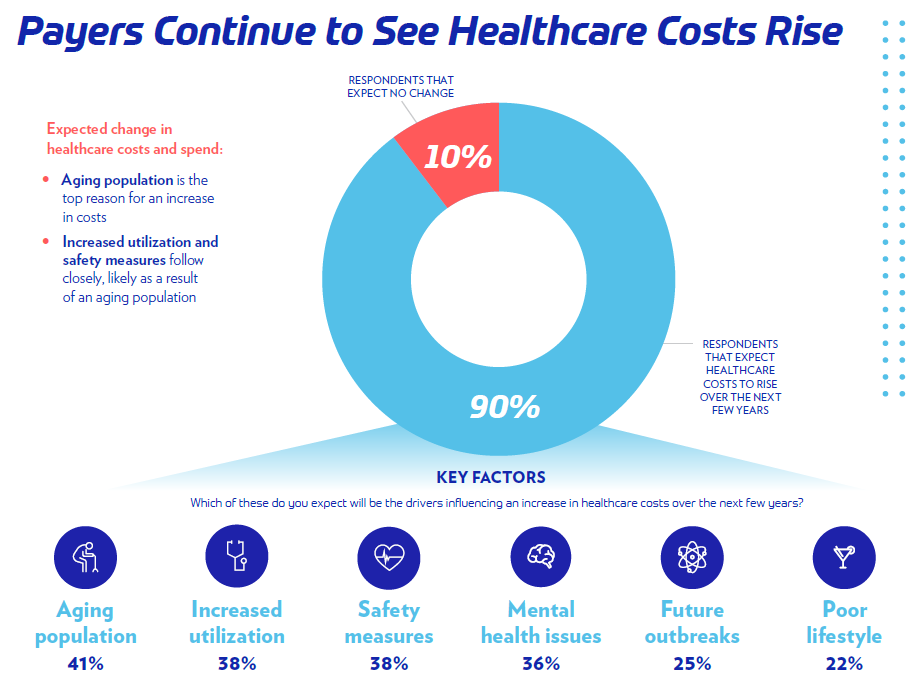

Payers continue to see healthcare costs rise, 90% of respondents expect healthcare costs to rise over the next few years.

While most patients would agree that healthcare costs are too expensive, there are certain demographic groups that feel it more than others.

- For instance, 86% of women think healthcare is too expensive,

- but only 74% of men agree,

- while 84% of those making less than $25,000 felt healthcare costs are too expensive compared to 75% of those making more than $100,000.

Artificial Intelligence / Machine Learning

Utilization of AI/ML initiatives across the healthcare industry remains in the early stages, but some stakeholders are starting to see the benefits.

Payers, specifically, are realizing a return on their investment with AI/ML:

- Nearly half of respondents reported a significant return,

- while most of the remaining majority broke even.

Additionally,

- 68% of health systems believe in investments in AI/ML will need to grow in order to meet enterprise goals, and

- four in 10 (40%¨) patients see AI/ML as beneficial to humanity.

Read more of the report’s most significant findings in the infographic.

________________________________________________________________

LONG VERSION OF THE REPORT

Executive Summary

IN THE 2021 STATE OF HEALTHCARE REPORT, HIMSS and its Trust partners — Accenture, The Chartis Group and ZS — offer key takeaways on current trends and challenges in healthcare, along with insights to drive real progress.

A phased approach was leveraged to develop the report. HIMSS conducted a series of 12 qualitative interviews with subject matter experts from across the health ecosystem to identify the most pressing challenges faced today.

Three of the highest priority areas — digital health, artificial intelligence (AI) and machine learning (ML), and financial health — were then used by the Trust partners as the starting point to design the quantitative approach.

The quantitative market intelligence in the State of Healthcare Report was collected from March to April 2021 and represents 2,743 respondents in the United States — 225 health systems, 309 clinicians, 147 payers and 2,062 patients. Participants answered a variety of questions relating to digital health, AI/ML and financial health.

Responses underscored the ever-shifting terrain surrounding healthcare access, data and costs in the United States. By better understanding these priority areas, stakeholders can bridge gaps, wisely invest limited time and resources, and plan for what’s next. Strategic planning will be vital as transformational trends in these three areas are poised to play pivotal roles in the healthcare industry for years to come.

By better understanding these priority areas, stakeholders can bridge gaps, wisely invest limited time and resources, and plan for what’s next.

Digital Health

The pandemic propelled digital health utilization to new heights, creating challenges throughout healthcare and promising lasting impacts.

By keeping close tabs on digital health trends, healthcare leaders can unearth future opportunities for innovation and proactively invest in the necessary tools and technology.

Health systems moved rapidly to establish telehealth offerings early in the pandemic and are now shifting focus to other use cases to gain a competitive advantage in this digitally advanced post-pandemic landscape.

- Most health systems offer digital programs,

- with nearly one-third having targeted, high-impact efforts that track key performance indicators and outcomes.

- However, 52% of providers have not progressed these initiatives beyond pilot stages.

The greatest barriers to adoption are not technology and patient demand; rather,

- 59% of respondents pointed to uncertainty over regulatory reimbursement issues and

- internal change management.

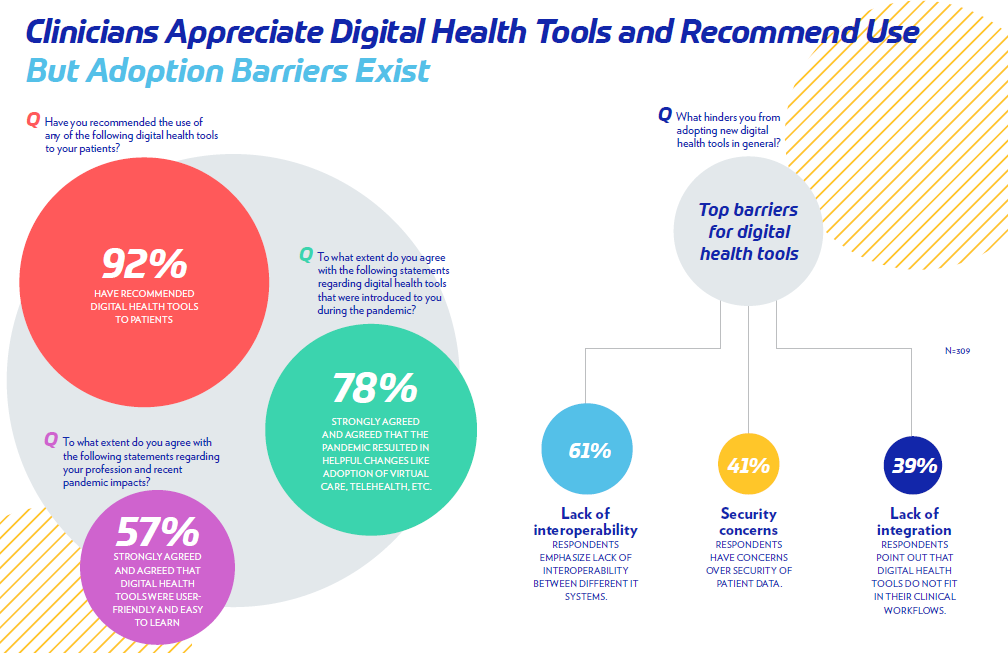

Clinicians adopted digital health tools at a faster pace during the pandemic, though more than 60% said the lack of interoperability between systems presents a hurdle.

- Amid security concerns surrounding digital health tools, more than eight in 10 clinicians trust their organization’s ability to protect patient health information, but this may be out of sync with the larger market as significant cybersecurity attacks continue.

- More than 90% said they have recommended digital health tools to patients and

- 78% agreed that the pandemic resulted in helpful changes like the adoption of virtual care, telehealth, and other tools.

Payers shared that the future of digital health will greatly rely on government regulations and payment reform.

- More than 60% pointed to interoperability of telehealth platforms as a driver to enhance adoption,

- though 40% cited privacy and security concerns as the top barrier.

Patients were often split by generational lines in their perception of digital health but will likely demand better remote options post-pandemic, with

- 71% of younger generations (Gen Z, millennials and Gen X) saying one reason they prefer telehealth is because of convenience.

- Gen Z and millennials are resisting a return to in-person care, with 44% saying they may switch providers if telehealth options aren’t offered going forward.

Artificial Intelligence and Machine Learning

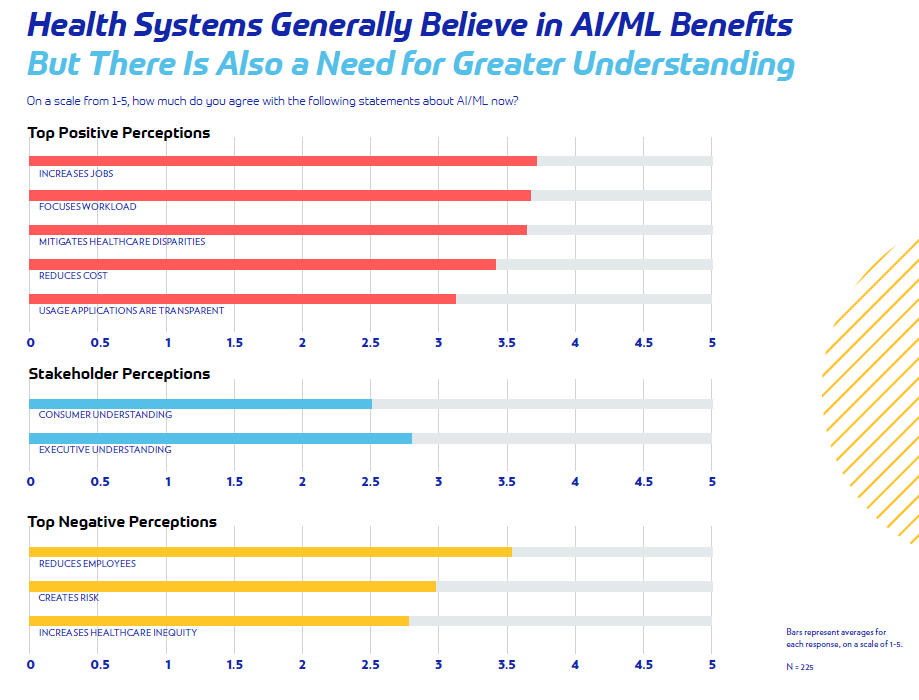

Utilization of AI/ML initiatives across healthcare is still relatively nascent, but segments are beginning to pinpoint key benefits amid lingering reservations.

Being sensitive to communities’ understanding and use of these technologies, as well as their concerns, can help leaders find and evaluate AI/ML opportunity areas while considering their organization’s existing assets.

Health systems believe (68%) they must grow AI/ ML investment to meet enterprise goals, yet 70% have yet to implement strategic AI/ML programs.

- Operational uses such as insurance, cybersecurity and fraud prevention rank highly in this group as viable AI/ML targets.

- Meanwhile, providers cited better-focused workloads as an important perceived advantage but are also concerned AI/ML might increase healthcare inequity and create risks.

Clinicians overwhelmingly (77%) are either using or interested in using AI/ML, contrasting sharply with the one in five who have received training in it so far.

This suggests an opportunity to share information and provide training for clinicians, 52% of whom cited better diagnosis as a top AI benefit.

Payers reported that today’s challenges to innovation are more technological in nature than cultural, with 62% saying that improving AI/ML capabilities and adoption are extremely high priorities.

Nearly half already have a dedicated innovation lab for AI/ML and enterprise-wide adoption.

Patients worry about organizations’ access to their personal health data, with nearly half resonating with a “big brother” sentiment in healthcare.

Despite their concerns, however, more than three-quarters are willing to share their health data for benefits such as

- early detection,

- more accurate diagnosis or

- better treatment.

Financial Health

Perceptions of financial health, particularly in the current state of the pandemic, depend largely on the segment’s specific role within the healthcare hierarchy and how they view the impact of an aging population.

Understanding critical challenges to the bottom line and the often-disparate views of alternate segments within the industry can help leaders pinpoint opportunities for greater efficiencies of care.

Health systems are prioritizing cost efficiencies and partnerships to help improve their financial position, perceiving other hospitals as their primary competitive revenue threat.

- While health systems still operate in a predominantly fee-for-service realm — with 68% of reimbursements coming through these arrangements —

- value-based care comprises a more significant share of reimbursement dollars than ever before.

Providers have also developed keen awareness of new competitors and potential market disruptors.

Clinicians report the pandemic’s financial impact as manageable:

- 70% described their current financial position as stable,

- with only 12% saying they’re somewhat or highly financially unstable.

Payers believe more reform is needed on payments and are focusing more intently on this as providers increasingly adopt value-based care arrangements.

- Payers cited an aging population as the top reason (41%) for an increase in costs,

- closely followed by a rise in healthcare utilization (38%) and

- safety measures (38%).

Patients overwhelmingly (79%) believe healthcare costs in the U.S. are too expensive, coinciding with payers’ perception that an aging population and increased utilization and safety measures are fueling growing costs.

- More than 80% of those making less than $99,000 per year have the strongest sentiment.

- On the other hand, 70% of patients are generally satisfied with their health insurance — particularly those from older generations — and agree that their healthcare insurance is a worthwhile investment.

- While older generations have the most favorable perception, most metrics tested were 50%+ favorable for all generations.

INDEX (Long Version of the Report)

- Health Systems

- Clinicians

- Payers 8

- Patients 10

1.Health Systems

Digital Health

Prior to 2020, digital health was gaining traction in the United States, but it wasn’t a primary focus for most health systems.

The COVID-19 pandemic, however, pushed the need for digital health options to the forefront.

“Now, there is broad recognition that digital is here to stay,” said Thomas Kiesau, director and digital leader for The Chartis Group, part of the HIMSS Trust partnership. “It was on everyone’s radar a couple years ago, but the pandemic really accelerated those programs.”

“It was on everyone’s radar a couple years ago, but the pandemic really accelerated those programs.”

In fact, the belief in digital is so strong that

- 70% of health system respondents said they have or are planning to establish a chief digital officer role.

- And eight in 10 providers (80%) currently have a patient portal in place — but not all are achieving the level of patient engagement that they desire.

What’s holding some systems back from adopting digital health is not technical issues — as many may think — but an overly complicated regulatory and reimbursement landscape.

“Regulatory questions aside, health system leaders are reasonably confident that technical and operational issues can be worked through,” Kiesau said.

Artificial intelligence and machine learning

When it comes to artificial intelligence and machine learning Kiesau said that most health systems acknowledge the opportunities that AI/ML present, but aren’t convinced of their value.

“People aren’t sure yet about it,” he said. “Operational business design is the easiest place to put it, and will likely drive the first wave of adoption.”

“People aren’t sure yet about it …” .

“Operational business design is the easiest place to put it, and will likely drive the first wave of adoption.”

From a financial health perspective, provider organizations still primarily operate in a fee-for-service world, though value-based care now comprises a more significant share of reimbursement dollars than ever before. And overall, other hospitals remain a health system’s top competitor.

“We need health systems to embrace and invest in profound organizational transformation,” Kiesau said. “Individual capabilities need to be improved.”

8 in 10 providers currently have a patient portal in place. But not all are achieving the level of patient engagement that they desire.

2.Clinicians

If there’s one word to describe clinicians coming out of the peak of the pandemic, it is resilient.

Clinicians have shown a tremendous amount of resiliency in this new normal,” said Darryl Gibbings-Isaac, MD, health strategy, growth and innovation expert at Accenture, part of the HIMSS Trust partnership. “They were really challenged and stressed by COVID-19, but they remain optimistic.”

In fact, 86% of clinicians said they are generally satisfied with their career and 65% said they’d recommend the profession to the next generation.

Clinicians also showed a strong interest in digital health — so much so that 92% of those surveyed said they’ve recommended digital health tools to patients.

However, adoption barriers still exist.

“A lack of interoperability, security concerns and a lack of integration were all barriers,” Dr. Gibbings-Isaac said. “If it disturbs the way they do work or if there are issues accessing appropriate data, for example, clinicians aren’t going to use it.”

“If it disturbs the way they do work or if there are issues accessing appropriate data, for example, clinicians aren’t going to use it.”

There’s also an openness to using AI/ML, but only one in five (20%) clinicians have received any training.

While a lack of trust in AI/ML developers was the greatest reason for hesitation, Dr. Gibbings-Isaac said he fully expects the number of clinicians using AI/ML to increase in the future.

Financially, the pandemic may have shaken many clinicians’ practice financials, but it wasn’t devastating. In fact, 70% of clinicians described their current financial position as stable.

“There was definitely an impact, but it seems to be flattening out,” Dr. Gibbings Isaac said. “Recovery is going to happen, and we can expect a more hybrid approach to medicine going forward.”

3.Payers

Payers are focused on three main areas:

- reducing healthcare costs,

- improving care quality and

- being prepared for a future pandemic or breakouts,

according to Shreesh Tiwari, principal, ZS, part of the HIMSS Trust partnership.

To assist in these endeavors, payers are looking to more advanced technology like AI/ML.

However, operational maturity — meaning outdated legacy systems — is an issue that will need to be addressed in order for AI/ML to be fully utilized. “Legacy technologies are a big concern,” Tiwari said. “They will create a barrier for driving innovation.”

Outdated legacy systems — is an issue that will need to be addressed in order for AI/ML to be fully utilized.

In fact, most of payers’ barriers to innovation today are technological, rather than cultural, in nature.

“By now, the cultural and mental barriers to technology have been overcome,” Tiwari said. “Now, it’s about creating efficient processes in order to realize ROI.”

Interestingly, data suggests that payers will rely on health IT startups, and big tech to drive technology innovations going forward.

“Traditionally, payers and providers have been the ones to drive innovation,” Tiwari said. “But now most payers believe that innovation will come from outside the ecosystem.”

Considering that, during the pandemic, providers who operated under value-based care (VBC) arrangements have fared relatively better than others, it’s encouraging to see an overall increase in provider adoption of VBC arrangements, Tiwari said.

“There is a strong level of forward thinking and optimism in the industry across business and IT in terms of leveraging technology to improve care,” he said. “This is so heartening to see because this is where the real innovation happens.”

4.Patients

From January to March 2021, two-thirds of patients visited a healthcare provider, despite the pandemic.

“Overall, the sentiment is that patients want to go back to pre-COVID-19 times when it comes to their healthcare experience,” said Lauren Goodman, director of market intelligence at HIMSS. “But this feeling isn’t specific to healthcare, it’s general pandemic fatigue.”

Convenience is what it all comes down to — 65% of all patients surveyed said they prefer telehealth because of the convenience compared to in-office visits.

But how much that convenience truly matters in the long run is, unsurprisingly, split among generations.

- Nearly half of millennials said they will prefer tele-health appointments once the pandemic ends, but

- only a quarter of baby boomer patients said the same.

Interestingly, more than one in three patients currently use some form of wearable technology to track things like heartrate, pulse, blood pressure and oxygen saturation.

However, the adoption rate of wearable tech for those whose annual household income is less than $25,000 is considerably lower.

“Based on the data, there is evidence that there are some serious health disparities and real issues with health equity,” Goodman said.

While 79% of patients believe that healthcare costs in America are too expensive, 70% also say that their health insurance is a worthwhile investment.

“With the pandemic, insurance companies have flexed and accommodated for patients, including possibly not charging for COVID-19 tests or telehealth visits,” Goodman said. “Additionally, are patients grateful that, in present times, they have health insurance? Transparently, it could be a mix of things.”

Overall, the sentiment is that patients want to go back to preCOVID-19 times when it comes to their healthcare experience.

HIMSS Trust Partnership

The HIMSS Trust partnership is a consortium of leaders from across the healthcare and technology space who are collecting, analyzing and reporting on in-depth, data-driven market intelligence. Insights gathered by the Trust will unveil trends and challenges to help the industry prepare and predict for the next three to five years.

Originally published at https://www.himss.org on July 28, 2021.