In the third quarter, the survey shows, incurred claims counts were 37.7% higher than a pre-pandemic baseline

The Wall Street Journal

By Leslie Scism

Updated Feb. 23, 2022 5:36 am ET

newscientist

U.S. life insurers, as expected, made a large number of Covid-19 death-benefit payouts last year. More surprisingly, many saw a jump in other death claims, too.

Industry executives and actuaries believe many of these other fatalities are tied to delays in medical care as a result of lockdowns in 2020, and then, later, people’s fears of seeking out treatment and trouble lining up appointments.

Industry executives and actuaries believe many of these other fatalities are tied to delays in medical care as a result of lockdowns in 2020, and then, later, people’s fears of seeking out treatment and trouble lining up appointments.

Some insurers see continued high levels of these deaths for some time, even if Covid-19 deaths decline this year.

In earnings calls for the past two quarters, Globe Life Inc., Hartford Financial Services Group Inc., Primerica Inc. and Reinsurance Group of America Inc. were among insurers noting higher non-Covid-19 deaths, compared with pre-pandemic baselines.

“The losses we are seeing continue to be elevated over 2019 levels due at least in part, we believe, to the pandemic and the existence of either delayed or unavailable healthcare,” Globe Life finance chief Frank Svoboda told analysts and investors earlier this month.

Among the non-coronavirus-specific claims are deaths from heart and circulatory issues and neurological disorders, he said. “We anticipate that they’ll start to be less impactful over the course of 2022 but we do anticipate that we’ll still at least see some elevated levels throughout the year,” he said.

Among the non-coronavirus-specific claims are deaths from heart and circulatory issues and neurological disorders …

Primerica executives similarly cautioned in their fourth-quarter call about outsize numbers of non-Covid-19 deaths in 2022. “Some of these will be the result of delayed medical care or the increased incidence of societal-related issues, such as the increased prevalence of substance abuse,” Chief Financial Officer Alison Rand said in an email interview.

From early stages of the pandemic, many medical professionals have raised concerns about Americans’ untreated health problems, as Covid-19 put stress on the nation’s healthcare system.

From early stages of the pandemic, many medical professionals have raised concerns about Americans’ untreated health problems,

Trade group American Council of Life Insurance said the pandemic in 2020 drove the biggest annual increase in death benefits paid by U.S. carriers since the 1918 influenza epidemic, totaling billions of dollars.

The hit to the industry’s bottom line has been less than initially feared, however, because many victims have been older people who typically have smaller policies, if any coverage.

Still, Covid-19 and other excess deaths have cut into many carriers’ quarterly earnings, especially as deaths linked to the Delta variant increased for people in their working years with employer-sponsored death benefits.

“Earnings impacts have been material and there still appears to be some Covid-19 discount, but investors are starting to look through mortality claims costs,” said Andrew Kligerman, a stock analyst with Credit Suisse Securities.

Industrywide, death-benefit claims usually vary only slightly year-to-year, so the recent increases are outside the norm.

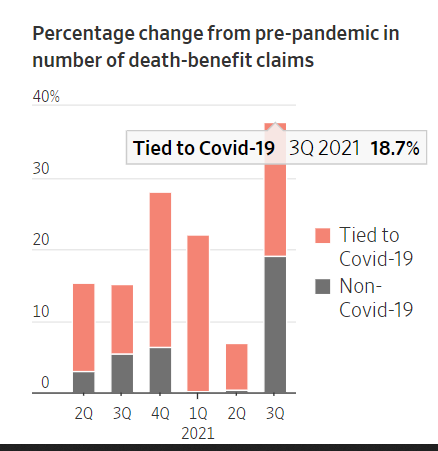

Non-Covid-19 excess deaths jumped in last year’s third quarter, after negligible or modest counts in earlier quarters, some life insurers said. Those numbers line up with results from an ongoing Covid-19 survey of 20 of the nation’s leading sellers of group-life insurance to employers by the Society of Actuaries Research Institute.

In the third quarter, the survey shows, incurred claims counts were 37.7% higher than a pre-pandemic baseline, with a nearly 50–50 split between claims directly tied to Covid-19 and those that weren’t, according to R. Dale Hall, managing director of research at the society, a professional organization. The group is still assessing fourth-quarter data.

In the third quarter, the survey shows, incurred claims counts were 37.7% higher than a pre-pandemic baseline,

The third-quarter non-Covid-19 excess claims were 19%, compared with 18.7% for Covid-19 claims, Mr. Hall said. Non-coronavirus-specific excess claims hadn’t topped 6.4% in previous quarters.

In discussing third-quarter results with analysts, Hartford Financial Chief Executive Christopher Swift said the company had “experienced higher levels of non-Covid excess mortality during the quarter,” including heart, stroke and cancer causes of death.

Among other insurance executives, Hartford Financial CEO Christopher Swift has noted an outsize number of benefit claims for non-Covid-19-specific deaths.

PHOTO: JULIE BIDWELL FOR THE WALL STREET JOURNAL

He said the company’s experience with such claims “has been very bouncy over the last six quarters so I don’t see a trend per se,” beyond those seeming “to indicate maybe a second-order effect with Covid and people not taking care of themselves.” The insurer is one of the nation’s biggest group-benefits providers.

At nonpublicly traded OneAmerica Financial Partners, another group-life-insurance seller, claims for working-age adults ran at about 140% of a pre-pandemic baseline during the third quarter, CEO J. Scott Davison said.

About two-thirds of these excess deaths are Covid-19-specific, he said. Of the remainder, in addition to deaths driven by deferred medical care, Mr. Davison’s team believes that some may stem from earlier Covid-19 infections.

He cited scientific research indicating that the virus may pave the way for future medical complications, so survivors may “later die from the toll Covid has taken on their bodies.”

He cited scientific research indicating that the virus may pave the way for future medical complications, so survivors may “later die from the toll Covid has taken on their bodies.”

The impact on the cost of life insurance from Covid-19 both directly and indirectly is unclear. Some insurers say they are repricing group-life contracts modestly on the assumption that the virus will be around at least through 2022. Those contracts are typically repriced every couple of years. Meanwhile, insurers are still trying to determine what implications there may or may not be on long-term mortality.

Originally published at https://www.wsj.com on February 23, 2022.