health transformation institute

the most comprehensive knowledge portal,

for continuous health transformation

Joaquim Cardoso MSc*

Chief Researcher and Editor, and Chief Strategy Officer (CSO)

November 25,2022

MSc* from London Business School — MIT Sloan Masters Program

Executive Summary

- We are currently facing a very difficult economic outlook.

- Our central scenario is not a global recession, but a significant growth slowdown for the world economy in 2023, as well as still high, albeit declining, inflation in many countries.

- Risks remain significant.

- In these difficult and uncertain times, policy has once again a crucial role to play: further tightening of monetary policy is essential to fight inflation, and fiscal policy support should become more targeted and temporary.

- Accelerating investment in the adoption and development of clean energy sources and technologies will be crucial to diversifying energy supplies and ensuring energy security.

- A renewed focus on structural policies will allow policymakers to foster employment and productivity, as well as to make growth work for all. In other words, it is in our hands to overcome this crisis.

- And if we choose to undertake the right set of policies, we will certainly increase our chances of success.

Infographic

ORIGINAL PUBLICATION (oecd)

Editorial: Confronting the Crisis

OECD

Álvaro Santos Pereira

OECD Chief Economist ad interim

22 November 2022

The global economy is reeling from the largest energy crisis since the 1970s.

The energy shock has pushed up inflation to levels not seen for many decades and is lowering economic growth all around the world.

In the new OECD Economic Outlook, we are now forecasting that world growth will decline to 2.2% in 2023 and bounce back to a relatively modest 2.7% in 2024.

Asia will be the main engine of growth in 2023 and 2024, whereas Europe, North America and South America will see very low growth.

In the new OECD Economic Outlook, we are now forecasting that world growth will decline to 2.2% in 2023 and bounce back to a relatively modest 2.7% in 2024.

In the new OECD Economic Outlook, we are now forecasting that world growth will decline to 2.2% in 2023 and bounce back to a relatively modest 2.7% in 2024.

Higher inflation and lower growth are the hefty price that the global economy is paying for Russia’s war of aggression against Ukraine.

Although prices were already creeping up due to the rapid rebound from the pandemic and related supply chain constraints, inflation soared and became much more pervasive around the world following Russia’s invasion.

As a consequence of the unexpected surge in prices, real wages are falling in many countries, slashing purchasing power.

This is hurting people everywhere.

If inflation is not contained, these problems will only become worse. Thus, fighting inflation has to be our top policy priority right now.

If inflation is not contained, these problems will only become worse. Thus, fighting inflation has to be our top policy priority right now.

Central banks around the world are increasing interest rates to curb inflation and anchor inflation expectations in their respective economies.

This strategy is starting to pay off.

For example, in Brazil, the central bank moved swiftly, and inflation has started to come down in recent months.

Central banks around the world are increasing interest rates to curb inflation and anchor inflation expectations in their respective economies.

For example, in Brazil, the central bank moved swiftly, and inflation has started to come down in recent months.

In the United States, the latest data also seem to suggest some progress in the fight against inflation.

Nevertheless, monetary policy should continue to tighten in the countries where inflation remains high and broad-based.

In the fight against rising prices, it is also essential that fiscal policy works hand-in-hand with monetary policy.

Fiscal choices that add to inflationary pressures will result in even higher policy rates to control inflation.

This means that policy support to shield families and firms from the energy shock should be targeted and temporary, protecting vulnerable households and firms without adding to inflationary pressures and increasing public debt burdens.

Governments have already done a lot to ease the economic pain from high energy and food prices, including price caps, price and income subsidies and reduced taxes.

However, since energy prices are likely to remain high and volatile for some time, untargeted measures to keep prices down will become increasingly unaffordable, and could discourage the needed energy savings.

Energy markets remain among the significant downside risks around this outlook.

Europe has gone a long way to replenish its natural gas reserves and curb demand, but this winter in the Northern Hemisphere will certainly be challenging.

The situation might be even more complicated in the winter of 2023–2024, as replenishing gas reserves might prove more difficult next year.

Higher gas prices, or outright gas supply disruptions, would entail significantly weaker growth and higher inflation in Europe and the world in 2023 and 2024.

Rising interest rates will also pose many challenges and risks.

Debt repayment will be more expensive for firms, governments and households who have variable rate debt obligations or when taking on new debt.

We are particularly concerned about low-income countries, over half of which are already in (or at high risk of) debt distress and now face tightening financial conditions.

Currency depreciation vis-à-vis the US dollar in many of these countries, and in emerging markets, adds to these risks.

Russia’s war against Ukraine is also aggravating global food insecurity by putting pressure on prices, supplies, and food affordability.

Some of the most vulnerable people around the globe face the highest risk of food insecurity, and many governments lack the means to address this problem.

Keeping markets open and agricultural goods flowing, as well as providing well-targeted aid, should be the utmost priority to avoid further food disruptions and hunger in many of these countries.

Policies for a stronger recovery

Policymakers must take bold policy actions to confront these challenging times.

In addition to monetary and fiscal policies, it is time for governments to go back to structural policies to tackle some of the most pressing current issues.

In addition to monetary and fiscal policies, it is time for governments to go back to structural policies to tackle some of the most pressing current issues.

First, investing in energy security and diversifying energy supplies is imperative.

To prevent energy disruptions, many countries are reverting temporarily to more polluting and carbon-emitting energy sources.

However, high energy prices and concerns about energy security are also encouraging governments and firms to diversify energy sources and boost investment in renewables.

Strengthening energy grids and investing in energy efficiency and green technologies will need to be high on political agendas to ensure that we reach our net zero emissions goals.

The OECD aims to support this effort through its Inclusive Forum on Carbon Mitigation Approaches (IFCMA), a forum of dialogue between countries at different stages of development that will allow us to better understand and analyse diverse policy approaches to carbon mitigation and their effects.

Second, governments need to keep markets open and international trade flowing.

This will strengthen competitive pressures and will help alleviate supply constraints.

In contrast, pursuing protectionist policies would be a serious setback for many countries, in particular the world’s poorest, and would significantly damage the global economy.

Third, fostering employment is essential to boost potential growth and achieve a stronger and more inclusive recovery.

For example, governments should work to decrease the gaps in employment rates between men and women in countries where these gaps remain high.

Investing in skills is also essential, to counteract the human capital losses that occurred during the pandemic, especially for the most vulnerable, and address the persistent and emerging skill shortages that many countries are facing.

22 November 2022

Álvaro Santos Pereira

OECD Chief Economist ad interim

1. General assessment of the macroeconomic situation

Introduction

The global economy is facing mounting challenges. Growth has lost momentum, high inflation is proving persistent, confidence has weakened, and uncertainty is high.

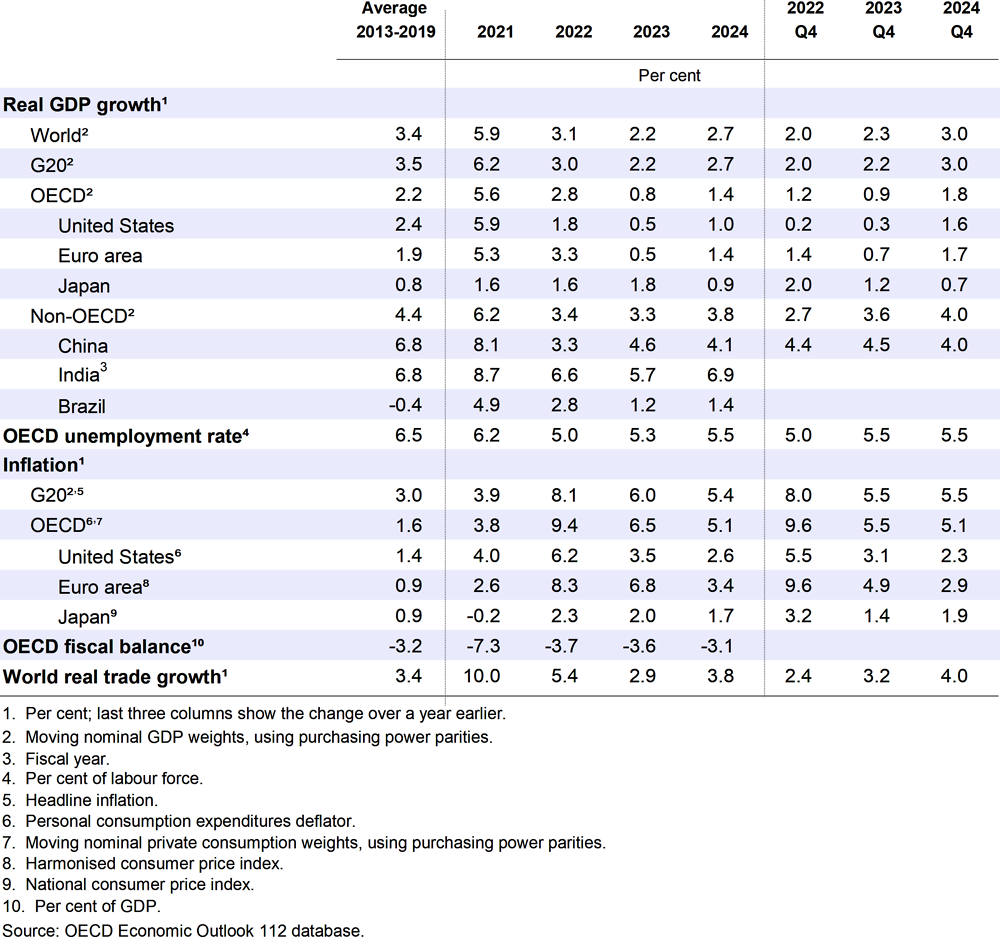

Russia’s war of aggression against Ukraine has pushed up prices substantially, especially for energy, adding to inflationary pressures at a time when the cost of living was already rising rapidly around the world. Global financial conditions have tightened significantly, amidst the unusually vigorous and widespread steps to raise policy interest rates by central banks in recent months, weighing on interest-sensitive spending and adding to the pressures faced by many emerging-market economies. Labour market conditions generally remain tight, but wage increases have not kept up with price inflation, weakening real incomes despite the actions taken by governments to cushion the impact of higher food and energy prices on households and businesses. Global GDP growth is projected to be 3.1% in 2022, around half the pace seen in 2021 during the rebound from the pandemic, and to slow further to 2.2% in 2023, well below the rate foreseen prior to the war. In 2024, global growth is projected to be 2.7%, helped by initial steps to ease policy interest rates in several countries. Global prospects are also becoming increasingly imbalanced, with the major Asian emerging-market economies accounting for close to three-quarters of global GDP growth in 2023, reflecting their projected steady expansion and sharp slowdowns in the United States and Europe. Headline consumer price inflation in the major advanced economies is projected to moderate from 6.3% this year to around 4¼ per cent in 2023 and 2½ per cent in 2024 as tighter monetary policy takes effect, demand pressures wane, and transport costs and delivery times normalise, although the pace of decline will vary across countries.

The uncertainty about the outlook is high, and the risks have become more skewed to the downside and more acute.

The projections reflect the toll taken by high energy prices over the next two years, but outcomes could be weaker still if there are energy supply shortages in global markets that raise prices further, or if enforced rationing is required to lower gas and electricity demand sufficiently during the next two European winters. Higher policy interest rates could also slow growth by more than projected, with policy decisions difficult to calibrate given high debt levels and strong cross-border trade and investment links that raise the spillovers from weaker demand in other countries. Widespread and rapid monetary tightening also heightens financial vulnerabilities. Financial strategies put in place during the long period of hyper-low interest rates may be exposed by rapidly rising rates and exert stress in unexpected ways. Many emerging-market economies could also face significant difficulties, particularly commodity-importing economies. Higher interest rates, the appreciation of the US dollar and a deterioration in the terms of trade increase the challenges of servicing elevated external debt and deficits, particularly if growth slows sharply and global financial conditions tighten further. Significant risks also remain about the projected steady expansion in China, with the continued weakness in property markets, rising non-performing loans and the disruptions from the continued zero-COVID-19 policy potentially weighing heavily on domestic demand and global growth. On the upside, reduced uncertainty, easier financial market conditions or lower commodity prices would moderate the slowdown in growth.

Elevated uncertainty, slowing growth, strong inflationary pressure and the ongoing impact of the war in Ukraine on energy markets leave policymakers with difficult choices in order to maintain macroeconomic stability and improve the prospects for sustainable and inclusive growth over the medium term.

- Continued monetary policy tightening is needed in most major advanced economies to anchor inflation expectations and lower inflation durably. Domestic policy measures will need to be carefully calibrated and responsive to new data given uncertainty about the growth outlook, the speed at which higher interest rates take effect and the potential spillovers from restrictive policy in other countries. Tighter global financial conditions and persistent inflation pressures are also likely to prompt further monetary policy tightening in many emerging-market economies, and limit the scope for any easing in countries where growth is slowing and interest rates have already been raised substantially.

- Fiscal support is being provided to help cushion the impact of high energy costs on households and companies. In the absence of such support there would almost certainly be sizeable output declines in many countries, with all of the attendant potential costs these could entail. However, better design is often needed to ensure support is only temporary and concentrated on the most vulnerable households and companies, preserves incentives to reduce energy consumption and can be withdrawn as energy price pressures wane. Short-term fiscal actions to cushion living standards should also take account of the need to avoid a further persistent stimulus to demand at a time of high inflation, thereby ensuring consistency with monetary policy and avoiding adverse effects on fiscal sustainability. Credible fiscal frameworks would help to provide clear guidance about the medium-term trajectory of the public finances and mitigate concerns about debt sustainability at a time of rising spending pressures and higher future payments on public debt.

- The war and the pandemic add to the longstanding challenges for growth, resilience and well-being from the acceleration of digitalisation, population ageing and the need to lower carbon emissions. Effective and well-targeted reform efforts are required to enhance productivity and skills, reduce inequality and improve gender balance, strengthen resilience and boost living standards. Well-chosen policies, such as increased support for childcare and reduced tax wedges for lower paid workers, could help to address the current pressures faced by lower-income households and also offer medium-term benefits for employment and inclusion. Keeping international borders open to trade, removing obstacles to stronger cross-border economic migration, and ensuring faster integration of migrants into the labour market would also help to alleviate near-term supply-side pressures on inflation. Governments also need to ensure that the goals of energy security and climate change mitigation are aligned. Efforts to safeguard near-term energy security and affordability through fiscal support, supply diversification and lower energy consumption should be accompanied by stronger policy measures to enhance investment in clean technologies and energy efficiency.

- The fallout from the war remains a threat to global food security, particularly if combined with further extreme weather events resulting from climate change. Better international cooperation is needed to keep agricultural markets open, address emergency food needs and strengthen domestic supply. Stronger international co-operation on debt relief, including through the G20, is also necessary to minimise the potential adverse economic and social consequences of default, with a rising number of lower-income developing countries already experiencing debt distress and having fragile banking sectors.

Table 1.1. Global growth is projected to slow further