IBM Institute for Business Value

September, 2020

Leading executives highlight five key opportunities that will help organizations respond to crisis and change.

When everything is a priority, nothing is a priority.

And as executives struggle to make sense of the post-COVID business environment, many find themselves leading from this gray area of indecision.

Two years ago, relatively few executives considered competencies in crisis management, enterprise agility, cost management, workforce resiliency, innovation, or cash-flow management as critically important to their business.

Today, however, top executives tell a different tale.

New research from the IBM Institute for Business Value shows that executives are now prioritizing all these capabilities.

In the next two years, our findings show that we should expect another huge shift in prioritization.

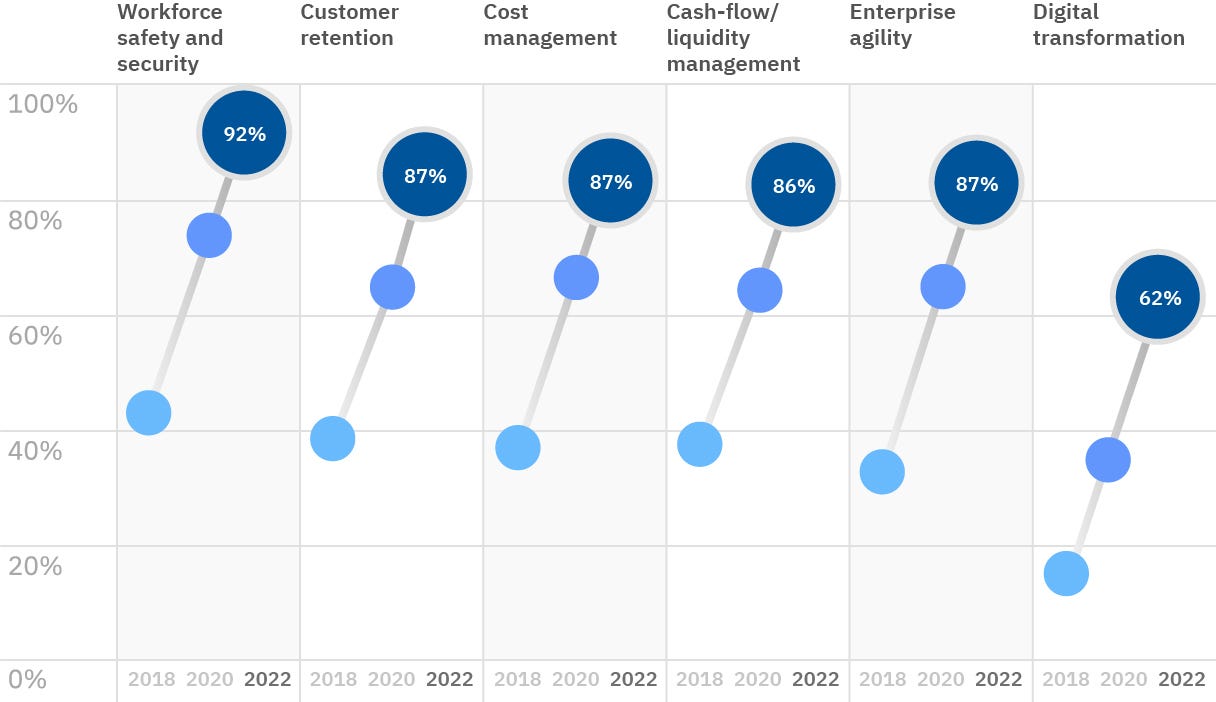

Executives are clearly telling us they plan to emphasize workforce safety and security, cost management, and enterprise agility.

Opportunities for a new era

Executives’ top priorities are shifting dramatically as they plan for an uncertain future.

Change remains the name of the game

Leaders are expecting more from their transformation initiatives.

They identify competitiveness and workforce resilience as the benefits they most want from ongoing digital transformation.

Transformation is also accelerating among a majority of organizations.

But strikingly, greater focus on transformation seems to be at the expense of customer relationships and partnering opportunities.

Executives identify competitiveness and workforce resilience as the benefits they most want from ongoing digital transformation.

This special IBV Trending Insights report integrates results from multiple proprietary surveys of consumers and executives conducted from April through August 2020, punctuated by new data from executives across industries who collectively oversee USD 3.7 trillion in revenue.

Our overwhelming conclusion: Post-COVID-19, the reality for businesses has radically shifted.

Whether reflecting on current conditions or future plans, business leaders’ needs for speed and flexibility have been amplified dramatically.

Old barriers are being brushed aside under the pressure of unrelenting disruption, rapidly evolving customer expectations, and an unprecedented pace of change.

There seems to be renewed clarity in their perspectives.

Motivation is not aspirational — it has become existential.

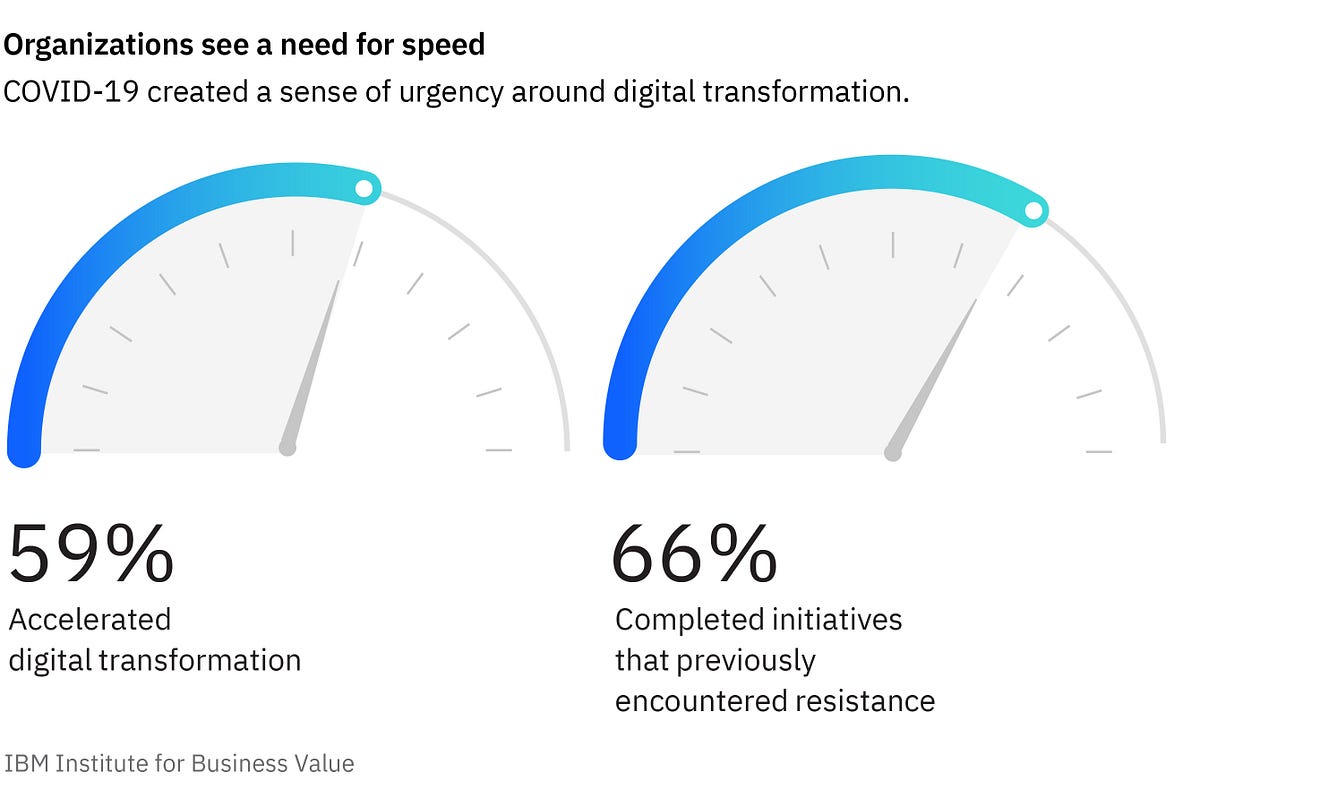

The COVID-19 pandemic has accelerated digital transformation at 59% of surveyed organizations.

Our research suggests five key epiphanies from leading executives for the post-pandemic business landscape, offering new perspectives on

- digital transformation,

- the future of work,

- transparency, and

- sustainability.

Together, they provide a playbook for proactive leaders who understand that old ways of working are gone.

- Epiphany 1: Digital transformation was never just about the technology

- Epiphany 2: The human element is the key to success

- Epiphany 3: Traumatic stress has hijacked corporate strategy

- Epiphany 4: Some will win. Some will lose. But few will do it alone.

- Epiphany 5: Health is the key to sustainability

Epiphany 1: Digital transformation was never just about the technology

Anecdotal tales of “game-time” pivots — moving swarms of workers to remote platforms, rethinking and remaking supply chains, shifting manufacturing to produce in-demand personal protective equipment — aren’t just near-term business contortions.

Adaptability is now a mandatory business competency, and an accelerated pace of change has become normal.

The COVID-19 pandemic has accelerated digital transformation at 59 percent of organizations we surveyed, and 66 percent say they have been able to complete initiatives that previously encountered resistance.

This culture shift is in part defensive: reducing costs is the top benefit attributed to transformation initiatives.

But something bigger and more long-lasting than crisis management is underway. Before the pandemic, many organizations seemingly distrusted their own technological capabilities and doubted the skills of their own workforces. Yet, in the blur of this year’s pandemic-induced reactions, those anxieties proved largely unfounded.

Executives have become more trusting of what technology can do, and they are pushing ahead with digital transformation.

Reliance on tech platforms became more acute, and those platforms — along with the corporate teams who use them — delivered results. It’s not that new tech was suddenly discovered and implemented; rather, the tools already at hand were deployed to fuller potential. Previous barriers to implementation were unceremoniously shoved aside, and those who moved first saw nearly immediate results.

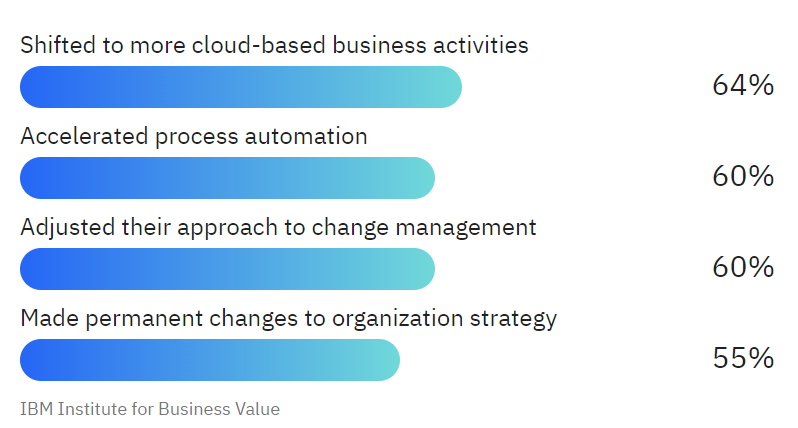

The COVID-19 pandemic has forever altered how organizations around the world operate. Some 55 percent of respondents say the pandemic has resulted in “permanent changes to our organizational strategy.” An even larger 60 percent say COVID-19 has “adjusted our approach to change management” and “accelerated process automation,” with 64 percent acknowledging a shift to more cloud-based business activities.

Defining a different normal

Organizations made big changes in response to the pandemic — and there’s no going back.

Executives have become more trusting of what technology can do, and they are pushing ahead with digital transformation. They indicate they are planning for COVID-19 recovery to include investment in technologies such as AI, IoT, blockchain, and cloud. The benefits long extolled by technophiles have become more broadly embraced across organizational leadership. To stack the deck for success, organizations need to be sure their people are as capable, resilient, and adaptable as their technologies for the long term.

Epiphany 2: The human element is the key to success

While executives plan to expand almost all tech competencies during their future digital transformations, the secret to success lies in human resources. In one IBV data set, our analysis confirms that the business competencies that account for the largest part of an organization’s expected growth are those centered around employees and customers, such as workforce training and customer experience management.

But remarkably, these factors seem to have eluded executives. More than three-quarters of executives expect changed customer behavior to continue after COVID-19, trading face-to-face contact for more shopping and customer service interactions online. To that end, 84 percent of executives say that customer experience management will be a high priority over the next two years, compared to only 35 percent just two years ago. And yet, “improved customer service” sits in the bottom half of the list of benefits that executives seek from digital transformation.

More than 3 in 4 executives expect changed customer behavior to continue after COVID-19.

This is curious, since 60 percent of executives also said they will employ AI-based customer engagement tools to achieve their goals, and in some organizations, chatbots are handling upwards of 80 percent of customer assistance traffic during the pandemic. We wonder how they will enhance customer experiences, if not at least in part through digital transformation.

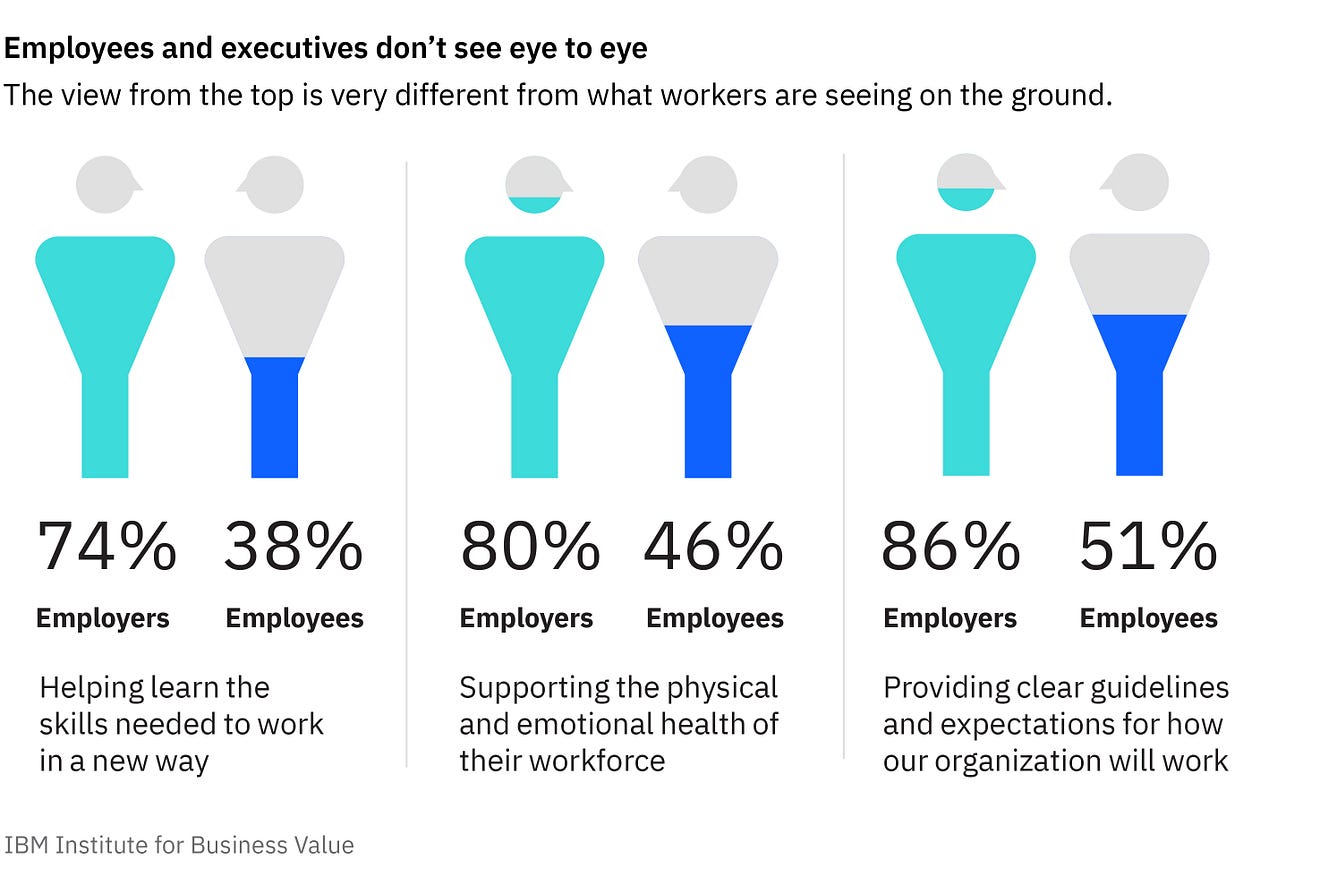

If executives are conflicted about how they’re connecting with customers, they’re doing even worse with their employees. While workforce safety, skills, and flexibility are important, employee satisfaction has been deprioritized. Executives recognize that their employees have been under intense pressure, and they contend that employee well-being is among their highest priorities.

Employers significantly overestimate the effectiveness of their support and training efforts.

But our research highlights a gaping chasm between what executives think they are offering their employees and how those employees feel: employers significantly overestimate the effectiveness of their support and training efforts. Only about half of employees say they believe that their employer is genuinely concerned about their welfare. Clearly, there is massive opportunity for leaders who can get this right, when most seem to be struggling.

This trust gap is not simply about perceptions. On the contrary, there is a reasonable foundation for employee skepticism about corporate commitment to them. According to our survey results, 22 percent of people have been either temporarily furloughed or permanently laid off since the pandemic began. Pair that with corporate priorities on cost-containment and technology resources — which are practical and even necessary — and employers may be sending signals that human resources are replaceable. Increased automation, AI adoption, and the emergence of other “contactless” activity reduce the number of people needed to do the work. In addition, the rising cost-management priority can hinder workforce support, work- from-home tools lag significantly behind needs, and the move to more remote work undercuts the personal connections that help define many corporate cultures.

Epiphany 3: Traumatic stress has hijacked corporate strategy

Executives are tasked with defining their organizations’ vision. But it can be hard to focus if they are continually putting out fires. While workforce safety and resilience, cost management, and organization agility emerge as top priorities for the short- and longer-term, the pandemic has amplified old business fears and introduced new ones. The result? Executives are enamored with the priority du jour.

Since the beginning of 2020, executive priorities have been a bit fluid, and they’ve reshuffled again the last few months. Now they seem to be focused on internal operational capabilities, which may be taking attention away from the customer service experience at a time when it could be critical.

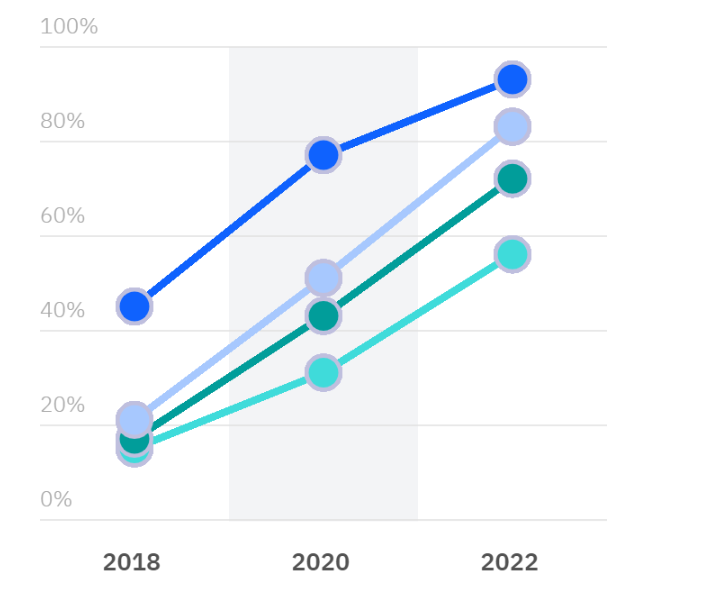

Executives are looking inward in the wake of COVID-19

Leaders plan to prioritize operational capabilities — not external growth — over the next two years.

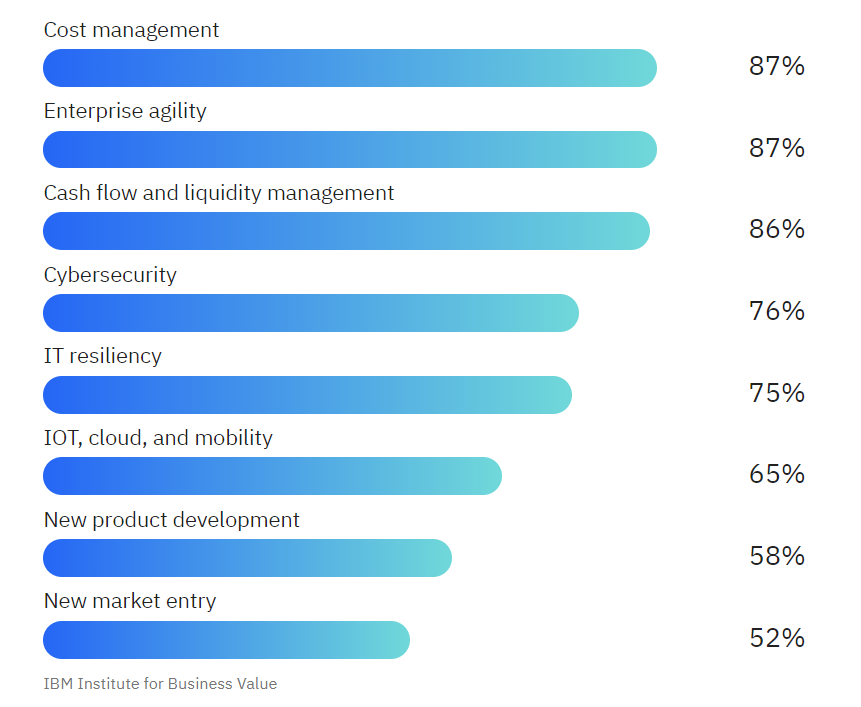

According to survey results from 3,450 executives in 20 countries across 22 industries, corporate priorities are much more focused on crisis management, workplace safety and security than they were two years ago. But in the future, 86 percent of executives expect cash-flow and liquidity management to be a priority — for more than twice as many respondents as two years ago.

In the same vein, 87 percent of respondents say cost control will be crucial. There is a heightened emphasis on resiliency, with 75 percent planning to prioritize IT resiliency over the next two years. And supply-chain reliability is of rising importance, with 40 percent of executives stressing the need for spare capacity to weather future crises, a telling move away from longstanding just-in-time-delivery goals.

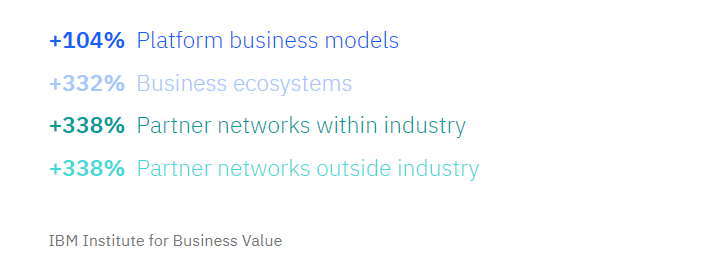

94% of executives surveyed plan to participate in platform-based business models.

Cybersecurity concerns have skyrocketed, too, with some industries showing an increased commitment of more than 90 percent. Overall, 76 percent of executives plan to prioritize cybersecurity over the next two years, with 46 percent planning to use AI to enhance cybersecurity in the same timeframe. That is twice as many as deploy the technology today.

Pre-COVID-19 commitment to business agility, AI, data and analytics, and other emerging technologies has grown. With the promise of competitive advantage now augmented by a new appreciation of the risks posed by crises, 87 percent of executives plan to prioritize enterprise agility over the next two years. More than 65 percent of respondents say investment in IoT, cloud, and mobility will be a priority; a whopping 94 percent plan to participate in platform-based business models.

So, everything is important. Everything except improving the customer experience — the one thing that can help drive performance and growth when the competition is lost in the fog.

Epiphany 4: Some will win. Some will lose. But few will do it alone.

The COVID-19 pandemic has not impacted all organizations and industries equally. This situation mirrors what some economists have described as a “K-shaped” consumer environment, where some thrive and others languish. The bifurcation in the stock market — where the biggest consumer tech platforms have steamed ahead while other shares drop — is just one indication of this divide.

Consider Amazon, which is up 78 percent this year. Its rise helped offset declines by more than half of the other companies in the consumer sector. Or look at Apple, which is up 60 percent and is now bigger than the bottom third of companies in the S&P 500 combined. The Amazons and Apples of the world may be examples of successful solo players, but most businesses need partnerships and ecosystems.

Scale alone doesn’t predict above-industry performance. The melding of size and flexibility is the defining characteristic of those poised for success.

Our findings show that executives expected health-related sectors to be the most likely post-crisis winners. Telecommunications, media, and entertainment were also expected to show positive impacts, buoyed by stay-at-home orders and habits. Atop the losers’ list: travel and transportation, and manufacturing-intensive industries, including automotive.

Within sectors, expectations are growing that broader reach will help define winners. Our data also point to greater reliance on platform business models and partner networks, with 70 percent of executives planning significant partnering activity inside their industry and 57 percent looking outside. Either way, they expect such participation to grow more than 300 percent over the next two years compared to two years ago.

Businesses are partnering up

Executives increasingly see platforms, ecosystems, and partner networks as key success factors.

The critical distinction here is that scale alone doesn’t predict above-industry performance. Large enterprises that can operate with agility have been the ones to remain steady (in a troubled sector) or outperform. The melding of size and flexibility is the defining characteristic of those poised for success.

There’s another point, too: When pandemic lockdowns were imposed, exceptions were made for services deemed essential — and “essential workers” became the most appreciated, cheered contributors in society. Alongside this heightened recognition of those who enable others to live, work, and play has been a refocusing on “the essentials” in all organizations and for all budgets.

A focus on growth and competitiveness demands renewed discipline around assessing and managing new business ventures and expansions.

Perhaps this explains why executives don’t expect to see benefits in these areas from digital transformation — it’s second-to-last on the list, behind only customer service. From an organizational perspective, a focus on growth and competitiveness demands renewed discipline around assessing and managing new business ventures and expansions.

In this time of disruption, it’s not a surprise that many, perhaps most, organizations have doubled down on their core — the operational improvements and workforce enhancements that may best address a returning crisis. And yet, executives must keep these hard-to-reach goals in their sights if they are sincere in their desire to increase competitiveness. These efforts are where tomorrow’s innovations and growth will come from. But approving and allocating resources for them will be scrutinized more than ever.

Epiphany 5: Health is the key to sustainability

Before coronavirus, sustainability strategies were largely centered on environmental issues: the risks to planetary health from pollution, climate change, and the like. Consumers were increasingly choosing products and brands that demonstrated authenticity in these areas, inspiring passion and allegiance. Regulators were echoing those concerns and priorities, as well.

Yet, faced with a human health crisis, environmental sustainability became joined with issues of personal safety. Consumers have been wearing disposable masks and gloves, and opting for more individual packaging than ever. To protect themselves and their loved ones from the virus, they’ve been receiving delivered goods to avoid going out in public. These actions seemingly pit protecting human health against protecting the planet.

But our research indicates that consumers’ passion for environmental issues remains. In fact, health and safety have been conjoined in a new, expanded, and more complex definition of sustainability. New burdens are already appearing for corporations, as they must make good on existing sustainability goals — reduced carbon footprints, more efficient waste management, or otherwise — while simultaneously meeting new health-and-safety requirements.

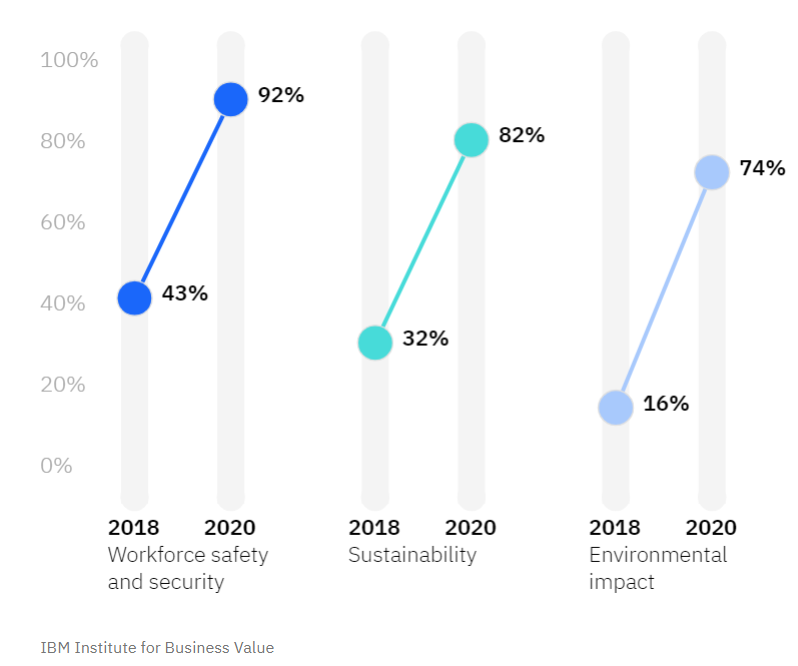

People and planet are inextricably linked

Executives’ concern for sustainability topics has skyrocketed in two years.

This may be among the more challenging — and critical — implications of post-COVID-19 business. Meeting this bar will require not only new practices and new materials, but also new kinds of data and efficiency. For example: What is the environmental cost of meat spoiling or being discarded versus using more plastic to make it safer? How do we enable supply chains and last-mile delivery to get what businesses and consumers require, without being needlessly wasteful? More sophisticated questions are coming, and leaders will be expected to provide more nuanced and educated answers.

Where to from here?

The pandemic was a wake-up call that the unexpected and the unlikely are more tangible and plausible than anyone previously anticipated.

For many, it has been a bitter reality: painful, costly, still unresolved.

For a few lucky others, it has offered an unforeseen windfall; one that organizations have struggled to capitalize on.

Either way, executives must accept that pandemic-induced changes in strategy, management, operations, and budgetary priorities are here to stay.

Accelerated investment is coming in digital tech, transformation, and cloud adoption.

We are on the leading edge of a self-reinforcing process, promising even greater acceleration ahead.

This presents an enticing opportunity for executives who can manage complexity and drive competitiveness by tying digital transformation to business priorities — while others are still waiting for things to “go back to normal.”

There is no going back to normal. The risks and opportunities are too great. The stakes are too high.

Organizational complexity remains the biggest hurdle to progress.

More than twice as many executives mention it as a barrier today as in the past.

Another related obstacle: employee burnout.

Data indicates that employees feel tired and overloaded, potentially as a reflection of that complexity.

All of this affords a new opportunity to build better businesses and a better world. It starts with enabling a diverse workforce to perform optimally — and building trust and confidence among employees will be critical.

How they are treated now will have an outsize impact on perceptions and value in the future.

Take action now

In the race for competitive advantage, it is imperative that organizations react in real time — that is, now — to navigate this new environment. Businesses need to take action in three critical areas in order to survive and flourish.

- Lead, engage, and enable the workforce in new ways with inspirational leadership. Provide support for more flexible work options (like hybrid models of remote and in-office work). Emphasize employees’ mental health and well- being, and skills development. All this can help in driving trust, binding the right talent to the organization long-term post-pandemic.

- Apply AI, automation, and other exponential technologies to make workflows more intelligent. Focus on supply chain resiliency, cybersecurity, and adoption of automation and AI.

- Improve operational scalability and flexibility, including the prioritized use of the hybrid cloud and moving more business functions to the cloud.

This new world permits no time for complacency or nostalgia.

There is no going back to what used to pass as normal.

The risks and opportunities are too great; the stakes too high.

Executives need to prepare their businesses for ongoing uncertainty, inevitable disruption, and never-ending change.

Originally published at