BCG — Boston Consulting Group

BCG Henderson Institute

By Martin Reeves, Philipp Carlsson-Szlezak, Kevin Whitaker, and Mark Abraham

April 3, 2020

COVID-19 and the containment policies aimed at controlling it have changed how we work and what we consume. History shows that such changes are not always temporary-crises can fundamentally reshape our beliefs and behaviors. How then can companies prepare for a postcrisis world, rather than hunkering down and waiting for a return to the past?

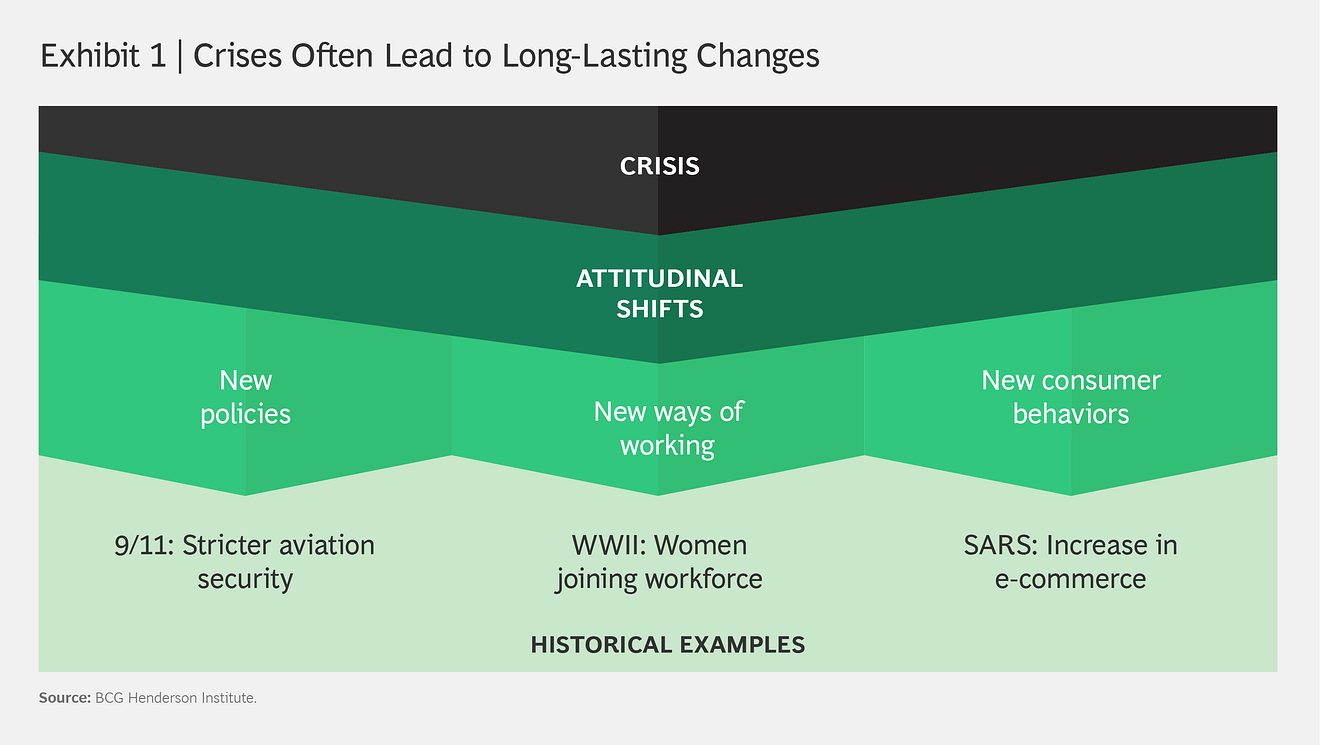

Let’s first consider how attitudes and behaviors are shaped by a deep societal crisis. Major disruptions can cause fundamental shifts in social attitudes and beliefs, which pave the way for new policies, ways of working, and consumer needs and behaviors, some of which persist in the long run. (See Exhibit 1.)

Historical Examples of Societal Crisis-Induced Shifts

The Black Death, which killed 25 million to 30 million people in 14th-century Europe, is credited by some historians with ending feudalism and serfdom and ushering in the Enlightenment by shifting power to increasingly scarce labor resources. We can say without exaggeration that the plague shaped the path of European history.1 Notes: 1 Walter Scheidel, The Great Leveler, Princeton University Press, 2017.

Consider also the impact of World War II on women’s participation in the workforce. With a large share of the working-age population deployed in the war effort, women were encouraged to fill jobs on the domestic front, through efforts to reduce social (and sometimes legal) barriers. After the war, the effects of these shifts persisted, driving an acceleration of female workforce participation.2 Notes: 2 Claudia Goldin and Claudia Olivetti, “Shocking Labor Supply: A Reassessment of the Role of World War II on U.S. Women’s Labor Supply,” National Bureau of Economic Research working paper, 2013.

The 9/11 terrorist attacks similarly reshaped transportation and security policies worldwide. There was a collective shift in societal attitudes about the tradeoff between personal privacy and security. As a result, citizens accepted higher levels of screening and surveillance in the interests of collective security.

Societal crises can also have lasting effects on consumption patterns.

For example, the 2003 SARS outbreak in China changed attitudes toward shopping: because many people were afraid to go outside, they turned to online retail. Though the crisis was short-lived, many consumers continued to use e-commerce channels afterward, paving the way for the rise of Alibaba and other digital giants.33 Notes: 3 Duncan Clark, Alibaba: The House That Jack Ma Built, Ecco, 2016.

How Will COVID-19 Shift Beliefs and Behaviors?

Lasting shifts in social attitudes, policy, work, and consumption will likely also emerge from the COVID-19 pandemic.

It’s hard to predict precisely how it will shape our perspectives on society, but it’s plausible that we could see a greater focus on

- crisis preparedness,

- systems resilience,

- social inequality,

- social solidarity, and

- access to health care.

It’s also easy to see how the crisis could accelerate nationalistic tendencies, and some commentators are already talking about the possibility of a “great decoupling” of international interdependencies.

At an individual level, it’s also possible that we may adjust how we view the balance between work and family life, having been reminded of what is truly important to us.

These attitudinal shifts could in turn be reflected in significant policy shifts in many areas, including trade, border controls, health care, crisis preparedness, foreign affairs, employment, and social welfare.

National security agencies are already drawing analogies between COVID-19 and cyber warfare, and rethinking and bolstering cyber defenses as a result. The pandemic could also shape national politics, as citizens judge the effectiveness of their governments’ responses.

Attitudes, policies, and the direct experience of the pandemic are already changing how we work, including greater emphasis on remote working, digital collaboration, workplace hygiene, and protections for temporary workers, for example.

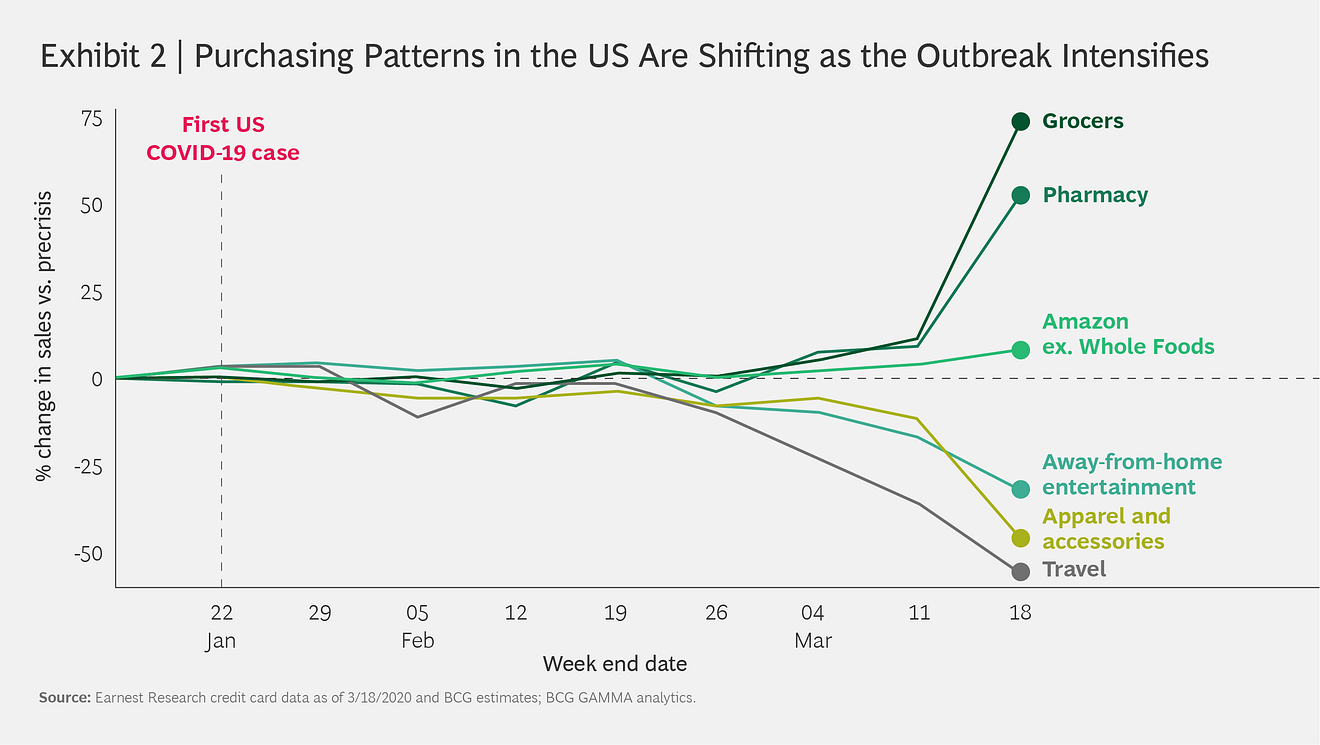

And we can already see significant shock-driven shifts in purchasing patterns in our analysis of credit card activity for hundreds of thousands of consumers. Groceries and pharmacy products have increased by more than 50% compared to pre-crisis levels, and online shopping on Amazon has also increased. On the other hand, travel spending has declined by 56%, and live entertainment and apparel purchases have declined by more than 30%. (See Exhibit 2.)

We should not expect that all of these shifts will stick, however.

For example, there was a marked reduction in air travel after the 9/11 attacks, but it returned to its previous trend line within 15 months. Undoubtedly we will see some consumption patterns reverting to long-term trend lines, albeit at different speeds. We must distinguish between temporarily postponed, accelerated, or disturbed consumption, and new, more permanent patterns of consumption.

Furthermore, we should not expect consumption to shift only among existing products.

New ideas often emerge or are developed in response to extreme needs arising during a social crisis.4 Notes: 4 Josef Taalbi, “What drives innovation? Evidence from economic history,” Research Policy, October 2017. World War II, for example, forced innovation or accelerated development and commercialization of the jet engine, pressurized aircraft cabins, helicopters, atomic technology, computers, synthetic rubber, rocketry, radar, and penicillin, with lasting effects. New needs born in our current crisis will likely drive lasting innovation in other areas, such as mass disease-testing technologies, digital collaboration tools, or affordable home office setups.

We should not, however, expect permanent shifts to be easily discernible through observation and analysis alone.

We cannot know for sure what shifts will persist until after the crisis is over, by which time pioneers will have already established leading positions. Pioneers will not only adapt to shifting needs; they will also proactively shape perceived needs and outcomes through innovation, education, and promotional activities.

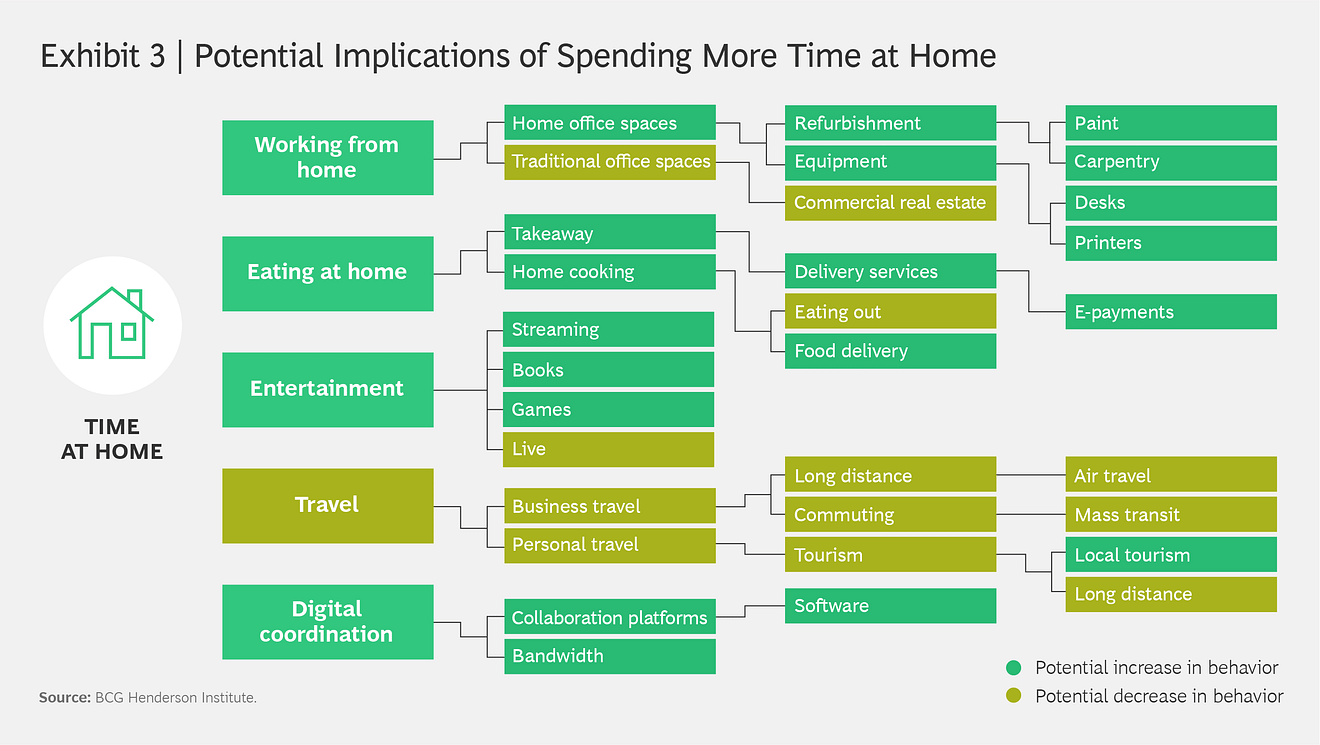

We can visualize the field of possibilities by observing fundamental attitudinal and behavioral shifts and creating branching trees of potential ramifications.

Fundamental shifts among consumers could include more time at home, more emphasis on hygiene and health, or greater emphasis on family security. Producer shifts could include embracing remote working, streamlining operations, decentralizing supply chains, and emphasizing crisis preparedness and systems resilience. Each of these basic shifts has manifold potential consequences. For example, the potential implications of increased time at home are shown in Exhibit 3.

It is too soon to know which of these possibilities will become firmly established. However, organizations can look to China for hints about which behaviors might stick. New infections in the country have slowed dramatically, social restrictions are being eased, and economic activity is restarting: as of late March, power consumption has recovered 80% of the way to last year’s levels and movement of people and goods has recovered 70%.5 Notes: 5 Power consumption measured by daily coal consumption at four major plants; movement of people and goods measured by average congestion delay index in ten major cities; source: WIND.

China has not returned to its precrisis state, however. According to a BCG survey, approximately half of Chinese consumers say they plan to spend more on preventative health care, vitamins and supplements, and organic foods over the next six months.6 Notes: 6 BCG COVID-19 Consumer Sentiment survey, March 12–16 (1,831 Chinese respondents). In contrast, more than one-third say they plan to decrease spending on restaurants, vacations, and tobacco products over the same timeframe. Such shifts are not guaranteed to last-with the outbreak still raging abroad and the possibility of a rebound in infections, consumers are likely still in a crisis mindset. Nevertheless, China will provide signposts to the shape of the post-crisis reality.

Divining and Shaping the Post-Crisis Reality

What practical measures can companies take to sense, exploit, and shape the post-COVID-19 reality? We suggest eight steps:

1.Expect change and look ahead.

Organizations tend to become myopic and insular when under threat. But crises often mark strategic inflection points, and a necessary focus on the present should not crowd out consideration of the future. The key questions become, what next, and with what consequences and opportunities?

2.Understand broader social shifts.

Addressable opportunities are often born out of new customer needs and frustrations, so listening to customers is vital. However, traditional surveys tell you only about existing product and category needs and uses; consumers may not be explicitly aware of their emerging needs. Companies need to look more broadly at how social attitudes are shifting to understand which observed changes in behavior and consumption could be lasting. For example, if leaders’ and workers’ attitudes toward remote working shift after a few months of experiencing it, that could have significant consequences for office equipment, office real estate, home remodeling, transportation, and other sectors and segments.

3.Scrutinize granular, high-frequency data.

Aggregates, averages, and episodic statistical data will not reveal the weak signals of change. Companies need to access and analyze high-frequency data, such as data on credit card transactions, at a very granular level in order to spot emerging trends.

4.Identify your own revealed weaknesses.

The crisis will undoubtedly expose needs for greater preparedness, resilience, agility, or leanness in different parts of your company. Those weaknesses also signal opportunities to renew your products and business model and serve customers better. They may also help you understand broader customer needs, since others are likely to be experiencing similar stresses.

5.Study regions further ahead in the crisis.

China and Korea are many weeks ahead of Western countries in their experience of crisis and recovery. By studying what happened in these markets, leaders can better predict which changes are likely to stick or could be shaped. A geographical fast-follower strategy may be available to agile players.

6.Scan for maverick activity.

Some companies, often smaller players on the edges of your industry, will be making bets predicated on new customer needs or behavioral patterns. Ask yourself, who are these mavericks, and which potential branches and leaves on the tree of possible shifts are they betting on? Are those bets gaining traction? What are you missing? From there, you can decide on the appropriate response to each opportunity or threat: ignore, investigate further, create an option to play, replicate and exceed, buy the maverick, or act with high priority.

7.Look at which new patterns reduce friction.

Frictions are unnecessary delays, costs, complexities, mismatches with needs, or other inconveniences that a customer experiences in using a particular offering. Forced habits that entail more friction than the traditional alternative are likely to be temporary: we may be forced to eat only canned food from our pantries in a crisis, but many are likely to return promptly to consuming fresh food when it is over. On the other hand, forced habits that reduce friction are more likely to stick: how many of us relish the thought of carving out a couple of hours each day to reach our workplaces? High-friction areas are also ones where it is logical for mavericks to innovate and where they are more likely to succeed.

8.Maintain hope and a growth orientation.

It’s almost inevitable that we will face a deep postcrisis recession. This is not a reason to postpone innovation and investment. Counterintuitively, 14% of companies grew both their top and bottom lines during recent economic downturns, and our analysis shows they create value mainly through differential growth. This is true across all industries. The evidence is clear: the best time to grow differentially is when aggregate growth is low. “Flourishers” in a downturn do reduce costs to maintain viability, but they also innovate around new opportunities, and they reinvest in growth pillars in order to capture opportunity in adversity and shape the postcrisis future.

About the authors

Martin Reeves

Managing Director & Senior Partner, Chairman of the BCG Henderson Institute

San Francisco – Bay Area

Kevin Whitaker

Head of Strategic Analytics of the BCG Henderson Institute

New York

Mark Abraham

Managing Director & Senior Partner

Seattle

Originally published at https://www.bcg.com on July 16, 2020.

Open the URL below to download the PDF

https://image-src.bcg.com/Images/BCG-Sensing-and-Shaping-the-Post-COVID-Era-Apr-2020-rev_tcm9-244426.pdf